Weekly Series: mREIT And BDC Recommendations (And Price Targets) As Of 07/04/2025

Summary

- Happy 4th of July! With the market closed, we’re celebrating with an early release of the article on our website.

- This is the first update since 6/20/2025, so it covers two weeks.

- We recently updated targets across the preferred shares.

- NYMT will be issuing a new baby bond with a 9.875% coupon rate. This one should trade as NYMTH. We will add the shares to our Google Sheets for members and open coverage (targets).

- BDC NAVs (net asset values) increased slightly. Prices increased a bit more.

In the exclusive section for full members:

- We’re including all the Q2 2025 estimates for earnings and book values (or net asset values for BDCs).

- We’re also including the dividend projections for each mREIT and BDC for Q3 2025.

- All of the current ratings and price targets, as we do each time we publish this article.

We aim to retain the same layout from week to week. I hope that makes it easier to find the parts that are most relevant to you.

Weekly Notes From Colorado Wealth Management Fund

Positions: 2 trades over the last 2 weeks.

- I purchased 1,239 shares of PMT-A (PMT-A) at $23.23 on 6/25/2025.

- I purchased 1,571 shares of PMTV (PMTV) at $25.11 on 6/27/2025.

Commentary: I’ve mentioned repeatedly that I intended to return to a more active position in preferred shares and baby bonds. A big part of that is purchasing positions. I’ll be actively trading in the sector much more because it’s typically been one of our best risk/reward opportunities. I would prefer to be doing it with prices for the sector being slightly lower, but the gap between what I want and where we are is only a month or two of income in most cases. Better to just get active and be making money.

Coverage on TWOD is still coming, as well as coverage on NYMTH.

Scott’s Ultra-Brief Summary

Most BDC NAVs likely slightly increased to close out the quarter. As such, BDC NAVs experienced a sharp decline in early April but most peers recovered most of their losses by quarter end. Regarding the mREITs, most agency mREIT BVs slightly - modestly increased from 6/20/2025 - 6/30/2025 (even when factoring in AGNC’s, DX’s, and ORC’s monthly dividend accrual). CHMI’s and NLY’s BV slightly decreased directly due to each company’s quarterly dividend accrual being fully realized. Excluding dividend accruals, BV increases were due to most agency MBS spreads modestly tightening versus underlying net (short) hedges. Most hybrid, originator + servicer, and commercial whole loan mREITs likely experienced relatively unchanged - slightly decreasing BVs this past week+. Again, the main culprit was the full realization of quarterly dividend accruals in most names. Excluding dividend accruals, most BVs would have slightly - modestly increased based on pricing/spreads/modeling.

Weekly Notes From Scott Kennedy

Positions: 0 trades over the past ~2 weeks.

In general, I am being patient regarding selectively deploying capital in attractively-valued mREIT common stocks with a less attractive risk/performance rating. My sector allocation to mREIT common stocks remains high (thus aligning with continuing to hold existing positions and selectively adding for future appreciation over the long-term). Patience remains key as catalysts/events will take time to play out (especially within commercial/multifamily mREITs). I will continue to remain disciplined regarding “picking and choosing” investments and lot sizes.

BDC Weekly Change: High yield/speculative-grade credit spreads slightly tightened over the prior ~2 weeks. This was mainly due to the apparent quick resolution regarding the U.S. air strike on Iran in late June 2025 and muted retaliation (calmed markets). As of early July 2025, we have continued to see a decent retracement in high yield/speculative-grade credit spreads after a very volatile April 2025. This is mainly due to continued optimism regarding tariff negotiations and semi-attractive economic data (inflation remaining fairly subdued, flat unemployment rate, etc…). Spreads moved back to relatively unchanged during calendar Q2 2025 (through 6/30/2025). As such, generally speaking, BDC NAVs likely rebounded a bit during June 2025.

BDC Other Comments (Current Week):

I will continue to monitor recent Middle East geopolitical tensions and monitor impacts in high yield/speculative grade markets as new events unfold. I continue to not anticipate any material/notable direct impacts to the BDC sector from these events. I am also monitoring upcoming U.S. economic data and monetary policy and impacts to the BDC sector.

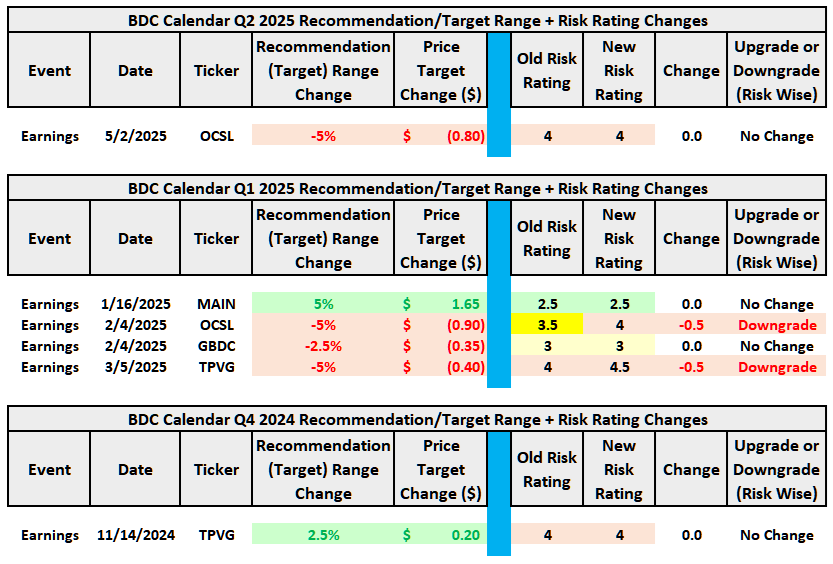

Calendar Q4 2024 + Q1 2024 + Q2 2025 Recommendation/Target Range + Risk/Performance Upgrades (Downgrades) (Running Tally):

Underlying Portfolio Company Credit Changes Held by BDCs (Weekly): 0 downgrades, 0 upgrades

Underlying Portfolio Company Credit Changes Held by BDCs (Quarter-to-Date):

This is a running tally of the credit upgrades and downgrades for companies held by each BDC (Bolded Indicates Current Week Change).