Prologis Q2 2025 Earnings Update

Prologis (PLD) delivered a good second quarter. It was a beat-and-raise. It’s hard to go wrong there. We've been invested in PLD for years and that's not likely to change.

My initial impression for the quarter was “favorable to slightly favorable”. I’m upgrading that to “favorable” upon getting a closer look at the line items.

Prologis Beats on Earnings

Core FFO of $1.46 beat estimates of $1.42.

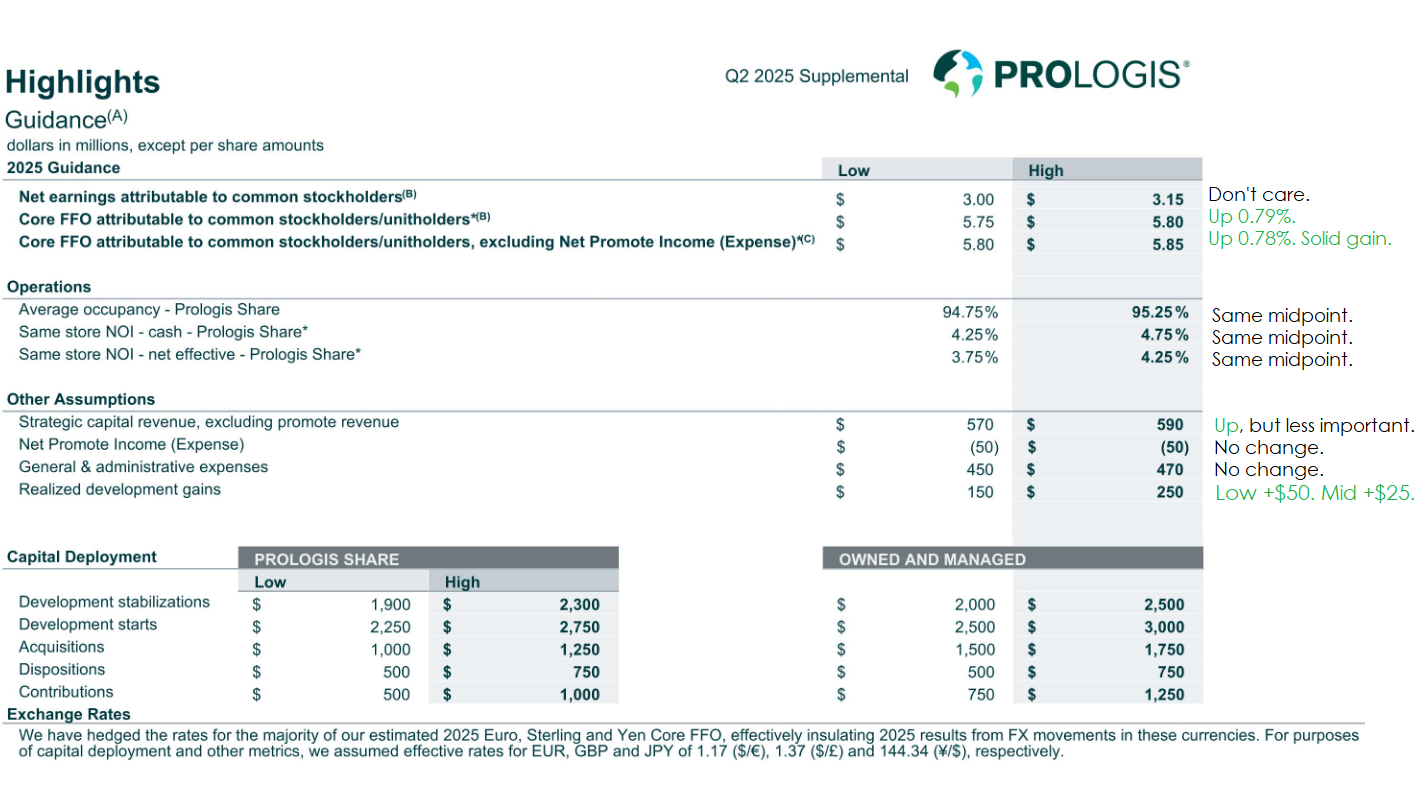

I grabbed an image to show the quarterly and annual projections.

The big question is what drove guidance higher? Specifically, if it was “Net Promote Income”, the increase in guidance would be less meaningful. That line can be quite volatile.

This image shows the guidance from Q1 2025 and Q2 2025:

There was no change in Net Promote Income projected, therefore this would most likely be either:

- Expectations for improved performance within the real estate or

- Reducing expected interest expense.

Since PLD doesn’t report guidance for interest expense as a unique line item in their supplemental, we’re looking at 2-year Treasury yields as a rough proxy. Those are slightly higher today than on 4/16/2025 when PLD provided their Q1 2025 earnings update. Therefore, the increased guidance is probably not driven by expectations for lower rates. That is good because we care more about the performance of the underlying real estate (where growth compounds) than about short-term fluctuations in interest expense.

I take the slide management provides for guidance and I add some notes on the right side to help investors interpret it quickly:

Increased Development

The capital deployment part (bottom part of the slide) is easier to visualize if you have a bigger table showing the guidance from each period and the change.

I prepared that table for our members: