Scott Kennedy’s mREIT + BDC Earnings Series: Assessing Rithm Capital’s And Oaktree Specialty Lending’s Performance For Q1 2024

Scott Kennedy’s mREIT + BDC Earnings Series: Assessing Rithm Capital’s And Oaktree Specialty Lending’s Performance For Q1 2024

Summary

This earnings assessment article reviews RITM’s and OCSL’s BV/NAV and core earnings/EAD/adjusted NII performance during Q1 2024 and compares results to expectations. Earnings remain a driver to stock performance.

RITM’s BV and adjusted core earnings/EAD matched my/our expectations (well within range). RITM’s BV slightly increased while the company’s adjusted core earnings/EAD was relatively unchanged.

No definitive updates by management on RITM’s potential spin-off (could be disappointing for some). No change in RITM’s percentage recommendation ranges or risk/performance rating. RITM is deemed slightly undervalued (BUY).

OCSL’s NAV also matched my/our expectations (well within range). OCSL’s adjusted NII slightly underperformed expectations (within range). OCSL announced a base management fee reduction (positive catalyst/trend).

Therefore, OCSL received a 2.5% recommendation range “upgrade” due to the projected increase in adjusted NII. No change in risk/performance rating though. OCSL is currently trading at my/our price target.

Formatting Change to this Article Series

We have recently changed the format of this earnings-related article series (less wording, more visual images). This process remains ongoing and future changes will likely occur.

1) RITM:

Commentary

Quarterly BV Fluctuation: Basically an Exact Match (0.1% Variance).

Adjusted Core Earnings/EAD: Basically an Exact Match ($0.005 Variance).

An “as expected” quarter regarding Rithm Capital’s RITM 0.00%↑ BV in my opinion. RITM recorded a minor BV increase which matched expectations. This is a pretty hard feat to accomplish when considering all the moving parts within RITM’s business model (numerous sub-portfolios), along with continued notable sector volatility regarding asset pricing and the various types of derivative instruments management utilizes at any given point in time (when considering agency MBS act as a hedge to the company’s MSR sub-portfolio). Let us briefly discuss how RITM’s segments/sub-portfolios performed when compared to my expectations.

First, RITM’s originations sub-portfolio had a modest increase in quarterly volume when compared to the prior quarter. RITM reported funded loan originations of $8.9 and $10.8 billion during Q4 2023 and Q1 2024, respectively. In comparison, I projected Q1 2024 funded loan originations of $9.5 billion (minor increase; factoring in historical seasonality). This resulted in a slightly larger net valuation gain on loans acquired for sale (including a similar GOS margin; 1.29% actual versus 1.25% projected). There was also continued strong loan originations within Genesis Capital.

Originations Summary (Includes GOS Margins)

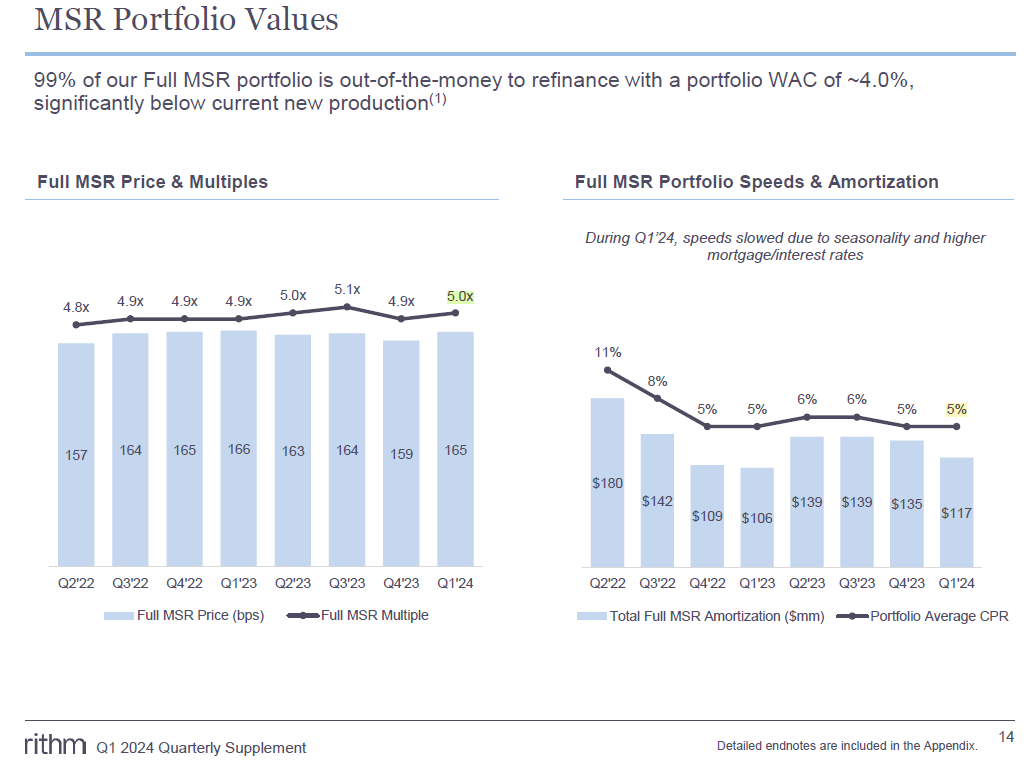

Second, the valuation fluctuations within RITM’s MSR sub-portfolio were largely as expected during Q1 2024. If anything, a very minor outperformance. When broken out, this included MSR amortization of ($117) million and “pure” valuation changes of $201 million (based on longer-term prepayment and default expectations). In comparison, I projected MSR amortization of ($125) million and “pure” valuation changes of $200 million. RITM’s MSR sub-portfolio experienced a quarterly increase in valuation multiple from 4.9x during Q4 2023 to 5.0x during Q1 2024. This matched my expectations.

MSR Valuation Multiple (Includes CPR Speeds)

Third, RITM notably increased the company’s highly liquid agency MBS sub-portfolio and continued to periodically call deals within the company’s non-agency residential MBS sub-portfolio. The amount of increase within RITM’s fixed-rate agency MBS sub-portfolio was a bit of a surprise and directly led to some more severe valuation losses when compared to my expectations. However, this was largely offset by an increase in RITM’s derivative instruments. Overall, a very minor underperformance when combining both sub-portfolios. RITM continued to allow roll-off within the company’s recently acquired consumer loans sub-portfolio (previously owned by an affiliate of Goldman Sachs) and very slightly increased its SFR sub-portfolio. RITM increased the company’s BPL sub-portfolio.

Fourth, RITM’s asset management revenues (mainly from Sculptor) slightly underperformed my expectations from a BV perspective (nothing “alarming”). Finally, RITM’s income tax (provision)/benefit account and equity accretion (dilution) basically matched my expectations. This can be one of those “quirky” accounts from quarter-to-quarter but no notable issues this quarter.

Moving on, RITM reported core earnings/EAD of $0.480 per common share for Q1 2024. However, when excluding a one-time benefit of $0.08 per common share in direct relation to the sale of capital assets (including excess MSR) during the quarter, RITM reported adjusted core earnings/EAD of $0.400 per common share for Q1 2024. Regarding excess MSR sales, these transactions are currently fully reversed out of taxable income and deferred back into taxable income over the remaining life of the applicable investments. Simply put, an “as expected” quarter for RITM on adjusted core earnings/EAD. Overall, RITM’s very minor decrease in quarterly adjusted core earnings/EAD was mainly due to the company’s modest increase in investment portfolio size (while continuing to keep credit risk “in check”) which was slightly “trumped” by a decrease in net spread income (lower-yielding assets) and an increase in operational expenses (even outside one-time expenses in relation the Sculptor/Specialized Loan Servicing [SLS] acquisitions). This was correctly anticipated.

A risk/performance rating of 3.5 for RITM remains appropriate in the current environment/over the foreseeable future as this mREIT can better combat (via the company’s MSR sub-portfolio) the “higher-for-longer” rates/yields scenario.

BV Performance (Actual Vs. Estimated)