Scott Kennedy’s BDC Earnings Series: Assessing Main Street Capital’s Performance For Q4 2023

Scott Kennedy’s BDC Earnings Series: Assessing Main Street Capital’s Performance For Q4 2023

Introduction section by Colorado Wealth Management Fund.

Article section by Scott Kennedy.

Bringing More of Scott’s Work to Our Website

The REIT Forum is a service produced by Michael Vanloon (better known as Colorado Wealth Management Fund) and Scott Kennedy. After intense consideration, I decided to launch our service through Substack. Since then, we’ve seen great success. Substack enables us to give readers real-time alerts with entire articles delivered directly to their inboxes.

You’re probably used to seeing the “from” field saying: “ColoradoWealthManagementFund from The REIT Forum”.

In some of our future e-mails, it may say:

“Scott Kennedy from The REIT Forum”.

That will simply mean we’ve updated the backend of the website for Scott Kennedy to directly post his articles.

I want to make browsing our work as simple as possible for readers. This will be another step in that direction.

For the moment, I’ll be posting Scott’s work. The following articles are a direct copy and paste from Scott. While we get the back end set up, there is a delay in getting the articles posted. Rest assured that it should be solved soon.

Finding Our Positions

I posted a subscriber-exclusive article with links to our Google Sheets. You can always access our positions there. Scott’s positions are updated each week. CWMF’s positions are usually updated on the same day as the trade.

Disclosures

Related to the stocks in this article:

CWMF is long: RITM-D, GPMT-A, DX-C, EFC-A, RITM-C, EFC-B, PMT-C, PMT-B, AGNCP, CIM-D, RITM-B, RITM, SLRC, GPMT, RC.

Scott Kennedy is long: RITM, RC, SLRC, GPMT, ARCC, GBDC, RITM-D, MITT-B, MITT-C, GAINL, ECCC.

The rest of this post is from Scott Kennedy.

Summary

This 2nd earnings assessment article reviews MAIN’s NAV and NII performance during Q4 2023.

This article also discusses how MAIN’s quarterly change in NAV and NII “matched up” to expectations. Earnings remain a key driver to stock performance.

MAIN’s NAV was a very minor-minor outperformance while its NII was a modest outperformance.

MAIN’s modest quarterly NII outperformance resides within the company’s dividend income account and/or a less-than-anticipated rise in non-accruals.

No change in MAIN’s percentage recommendation ranges or risk rating. MAIN is currently deemed slightly overvalued (SELL). MAIN remains a very good BDC from an operational standpoint but remains "pricey".

Introduction:

Hi subscribers. For new members, my name is Scott Kennedy and currently I fully cover 20 mortgage real estate investment trust (mREIT) and 15 business development company (“BDC”) common stocks within this Investing Group regarding research/data, subscriber questions, weekly projected book values/net asset values (BV/NAV), and common stock recommendation ranges. Colorado (“CO”) Wealth Management handles the mREIT preferred stocks and he and his team handles all other applicable REIT sectors outside the mREIT sector. CO also provides some mREIT common stock and BDC articles from time-to-time which are more of an “overview/introduction” discussion; typically based either on my or our combined research/data. This also includes some macroeconomic trends and data. My name is always attached to all Investing Group articles I personally wrote so there is no confusion for subscribers.

This REIT Forum article is part of a series of articles over a span of 6-7 weeks which will analyze my previously projected BV/NAV and core earnings (or core earnings equivalent)/net investment income (“NII”) figures and compare these metrics to each mREIT’s and BDC’s actual reported results, respectively. For readers who are familiar with my public mREIT and/or BDC articles, these types of articles are beneficial to readers who desire to pursue a more active investing strategy and/or want more “real time” thoughts/analysis.

I hope my services/contributions ultimately help enhance a subscriber’s total investment returns or minimize their total investment losses within the mREIT and BDC sectors. At the very least, I hope subscribers will gain more insight into the mREIT and BDC sectors by reading my/our exclusive REIT Forum articles.

1) MAIN’s NAV and NII Q4 2023 Performance (Projected Versus Actual Results):

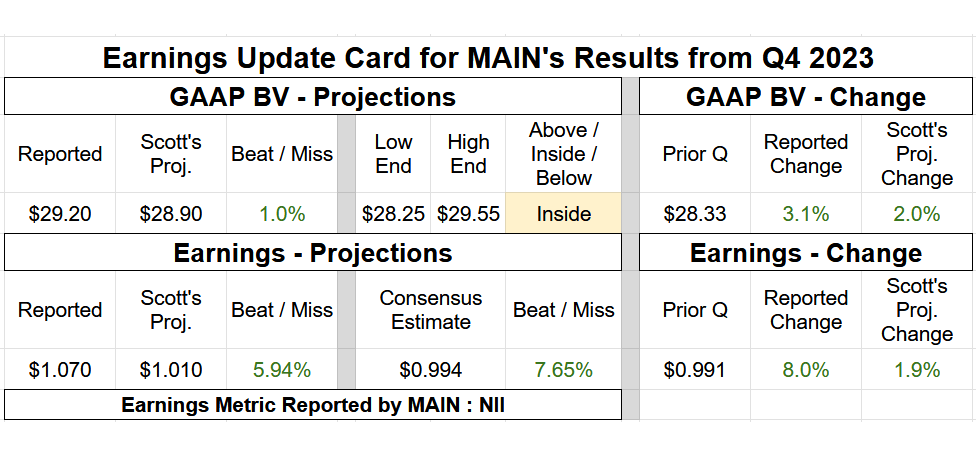

On 1/17/2024, Main Street Capital Corp. (MAIN) reported the company’s preliminary earnings results for the fourth quarter of 2023. Table 1 below provides MAIN’s NAV and earnings summary.

Table 1 – MAIN Q4 2023 NAV and Earnings Summary

Source: Taken Directly from the REIT Forum’s © Analytical Spreadsheets/Data

I am providing the following commentary in regards to MAIN’s preliminary results for the fourth quarter of 2023:

“Hi subscribers. I was able to review MAIN's Q4 2023 preliminary earnings results that were disclosed earlier today.

MAIN reported an estimated net asset value (“NAV”) range as of 12/31/2023 of $29.17 - $29.23 per share (3.0% - 3.2% increase) versus my prior projection of $28.90 per share (2.0% increase). I consider the mean of this estimated range, $29.20 per share (3.1% increase), a minor (greater than a 1.0% but less than a 2.5%) outperformance and was within my $28.25 - $29.55 per share range. As is typically the case, the majority of this quarterly NAV increase was directly in relation to MAIN’s use of the company’s “at-the-market” (“ATM”) equity offering program. When MAIN’s stock price continues to trade at a notable premium to CURRENT NAV throughout the quarter, it is a great luxury to issue shares of common stock at a cheaper cost of capital when compared to sector peers (which has been factored into MAIN’s percentage recommendation ranges and risk rating for many years now). MAIN also recorded a quarterly tax benefit during the fourth quarter of 2023 which very likely led to the vast majority of the company’s quarterly NAV outperformance when compared to my expectations (a bit of a surprise; likely due to net realized losses being generated during the quarter). Still, until MAIN officially reports earnings for the fourth quarter of 2023, I cannot fully reconcile the company’s very minor - minor NAV outperformance.

As of 9/30/2023, MAIN had 12 portfolio companies on non-accrual status. I anticipate continued credit risk/portfolio pressure on a couple other lower middle market (“LMM”) investments which have been highlighted in our weekly mREIT and BDC recommendation article series over the past several quarterly cycles. Credit risk will remain a key metric to track over the foreseeable future. Since MAIN mainly invests in the LMM, credit risk/non-accruals are just “the name of the game”/typical. Simply put, there is a higher risk of non-accruals in some portfolio companies but there is also the eventual possibility of higher rewards through notable LMM equity appreciation in other portfolio companies (via growth over time).

In addition, MAIN estimated the company's net investment income (“NII”) for the fourth quarter of 2023 was in a range of $1.060 - $1.080 per share. This calculates to a quarterly increase of $0.069 – $0.089 per share. In comparison, I previously projected MAIN would report NII of $1.010 per share for the fourth quarter of 2023 (a very minor increase). As such, this was a nice “bounce back” in MAIN’s quarterly NII when compared to the modest decrease recorded during the third quarter of 2023 (greater increase versus what I [and the institutional analysts] projected). Since quarterly loan originations and minor net portfolio shrinkage across MAIN’s 3 combined investment sub-portfolios came in largely as anticipated, the likely quarterly NII outperformance resides within the company’s dividend income account and/or a less-than-anticipated rise in non-accruals. Unlike most BDCs, a pretty large proportion of MAIN’s NII is derived from recurring quarterly dividend income via the company’s many equity positions in control and affiliate investments (over 100 companies). As such, it will be interesting when MAIN provides the company’s full earnings report next month. I/We perform a “deep dive” within all facets of MAIN’s operations, including underlying dividend income trends/forecasting on all control and affiliate investments. I will let subscribers know, if deemed material, where notable dividend income variances occurred regarding specific portfolio investments.

From the disclosed results today (mainly MAIN’s estimated NAV range as of 12/31/2023 and NII estimated range for the fourth quarter of 2023), along with macroeconomic trends/events (mainly Fed monetary policy, the general projected movement of rates/yields, and projected economic performance over the foreseeable future), no change to my/our MAIN percentage recommendation ranges (relative to CURRENT NAV) or risk rating (remains at a 2.5). As noted last quarter, when MAIN’s NII modestly decreased, I deemed it was unwarranted to perform a percentage recommendation range downgrade. Simply put, I anticipated a better NII performance during fourth quarter of 2023 and MAIN did not disappoint. This more favorable quarter was already anticipated and factored into MAIN’s percentage recommendation ranges.

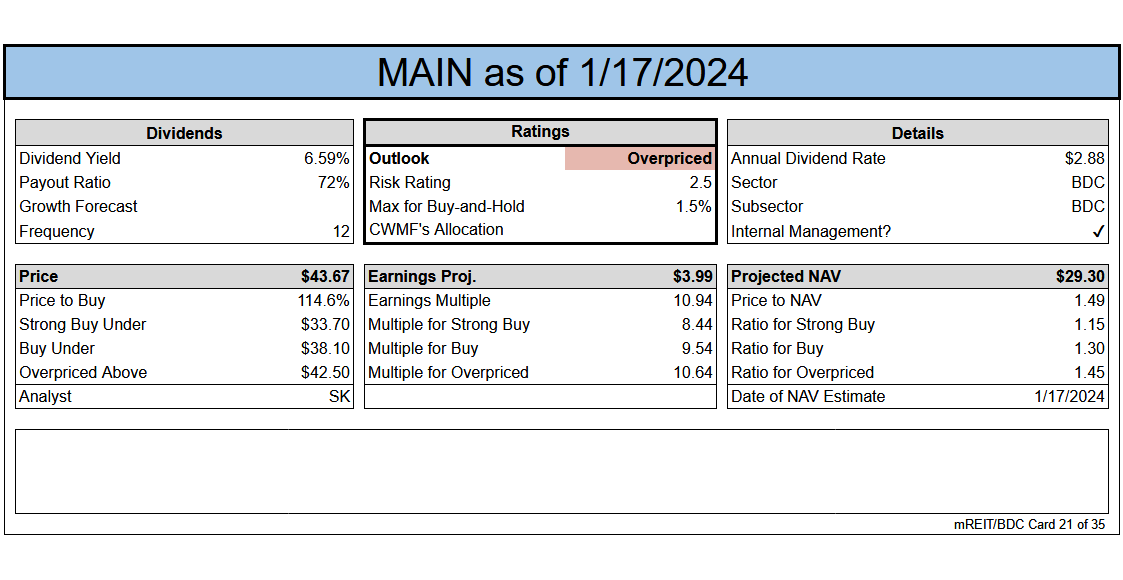

MAIN will, once again, outperform most (if not all) sector peers regarding quarterly NAV fluctuations. MAIN remains a very well-run, and well-performing, BDC. The typical issue with MAIN is valuation (usually pricey – very pricey). Currently, MAIN is trading at an approximate 49% premium to our CURRENT NAV per share projection. While certainly not as high as some historical premiums north of 70%, just not as low/attractive a premium of only 27.5% - 32.5% that occurred during the fall of 2022.

Remember, as MAIN continues to gradually grow NAV over time, the company’s per share price targets will move in “lock step” to said movement. What we try to accomplish with MAIN, regarding investment strategy, is to invest in shares at an attractive valuation when there are market dysfunctions which results in a quick, sharp decline in stock price. Yes, investors have to have a good deal of patience regarding this specific strategy during certain interest rate and credit/market cycles. However, as shown in the past, this disciplined approach has directly led to notably more enhanced total returns on one’s MAIN investment. In the meantime, there are other sector peers that are trading at a more attractive valuation which provide a higher annualized yield.

At a closing price as of 1/17/2024 of $43.67 per share, MAIN is deemed to be slightly OVERVALUED/a SELL recommendation (price target of $42.50 per share). While the fairly recent rapid increase in LIBOR/SOFR/PRIME has been a net positive for MAIN (and the BDC sector as a whole regarding NII growth), I continue to believe sector-wide NII’s are at or nearing their peak this interest rate cycle (outside merger benefits/cost saving measures/management + incentive fee reductions). I also continue to believe recessionary/credit risk will be on the rise over the foreseeable future. As such, a bit of caution in general (which is already reflected in sector recommendations/pricing)…”

Conclusions Drawn + BUY, SELL, or HOLD Recommendation:

Readers have continued to request that I provide these types of “earnings assessment” articles showing how my previously disclosed quarterly projections “stacked-up” to each covered mREIT’s/BDC’s results. I believe the analysis above accomplishes this request for the REIT Forum subscribers.

In summary, here is how MAIN performed when compared to my expectations regarding the fourth quarter of 2023 (includes any risk rating and BUY, SELL, or HOLD recommendation range changes; as well as current recommendation):

1) MAIN

NAV: Very Minor-Minor Outperformance (Within Range)

NII: Modest Outperformance (Slightly OUTSIDE Range)

Percentage Recommendation Range (Relative to CURRENT NAV): No Change (Reasoning Provided Above)

Risk Rating: No Change

Table 2 – MAIN Notecard (As of 1/17/2024)

(Source: Taken Directly from the REIT Forum’s © Subscriber-Accessible Spreadsheets. Earnings Projection is Taken Directly from Either the Prior Quarter’s Actual Reported Figure or the Institutional Analysts’ Consensus Average and Annualized. At the End of Each Current Quarter, I Provide My Own Finalized Core Earnings/Core Earnings Equivalent or NII/Adjusted NII Metric Which Will Differ from the Estimate Provided Above.)

Important Note: As always, please check the Google shared spreadsheets when it comes to intra-week recommendations as stock prices fluctuate.