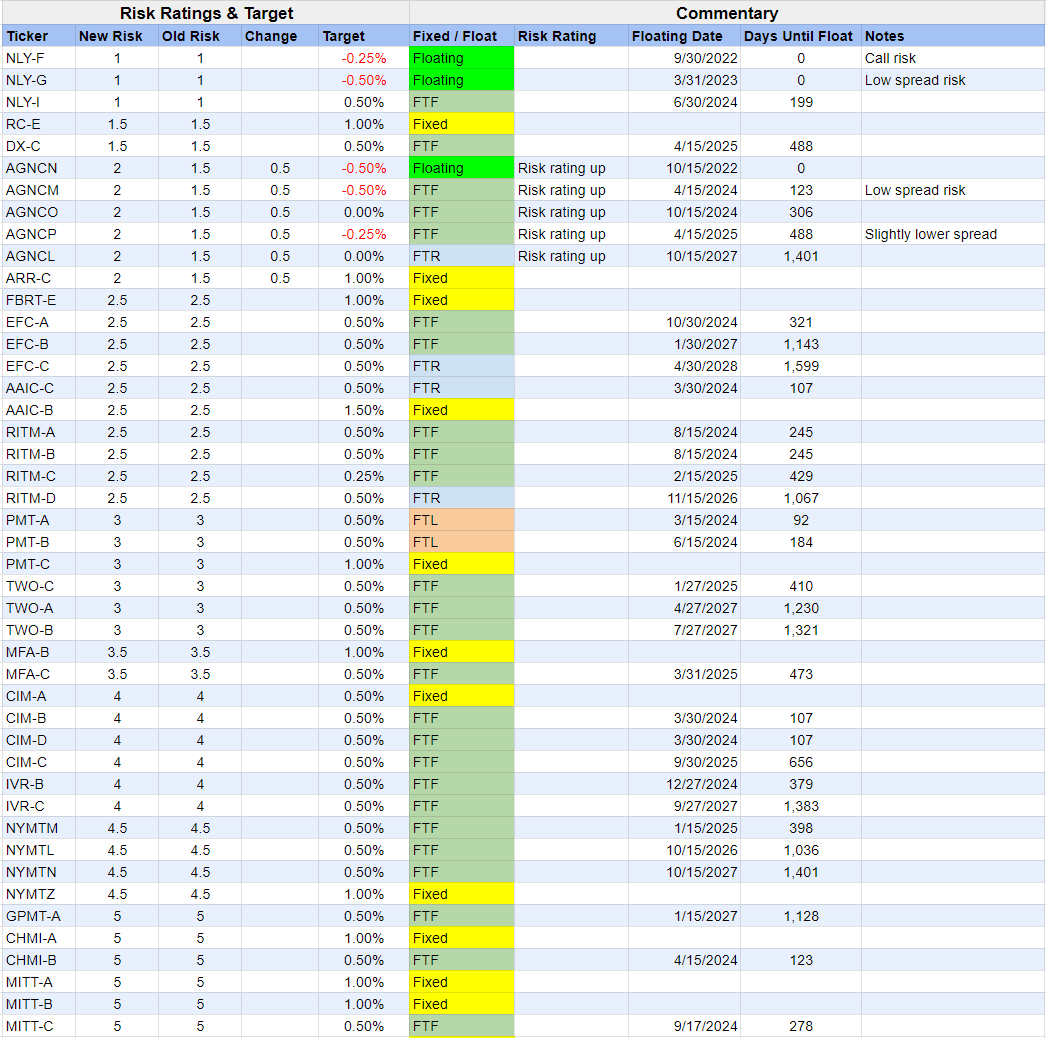

Preferred Share Target Updates

We’ve got a bunch of preferred share target updates.

None are huge, but they will create a bit of a shift in relative rankings.

We’re adjusting for a few things.

AGNC preferred share risk rating update as previously foreshadowed to members.

Adjustment for shares that are already floating. The expected dip in short-term rates may reduce enthusiasm.

Adjustment for shares with lower floating spreads. Based on expected dips in short-term rates, lower spreads will be a bigger factor. NLY-F vs NLY-G is a good example. After further inspection, I might adjust these a bit further.

Adjustment for shares that are not yet floating. Even though projected short-term rates are down, the shares are moving closer to big dividend increases. Targets go slightly higher.

Adjustments for fixed-rate shares. The reduced long-term rates (IE: 10-year Treasury) result in a little boost to targets. Investors are still looking for a combination of a respectable yield and extra upside (if rates fall further). These shares tend to have some of the bigger discounts, so they have more upside if rates continue to fall.

The adjustments are included below:

Terms:

Floating = Shares are floating.

Fixed = The dividend rate is fixed indefinitely.

FTR = Fixed to Reset. These shares eventually begin resetting the dividend rate based on the spread + the 5-year Treasury rate.

FTF = Fixed to Floating. These shares switch to 3-month SOFR.

FTL = Fixed to Lawsuit. This is how I note shares where management is attempting to claim the shares will remain fixed rate. I am not a lawyer. My assessment that management is wrong is based on my research and supported by announcements from CIM and TWO. Both REITs had shares with very similar wording and determined that by law the shares must float based on SOFR.

Quick explanation for AGNC and NLY shares:

NLY-G and AGNCM had some negative adjustments because they have thinner credit spreads. AGNCP has a slightly thinner spread than other shares. However, AGNCP’s spread is better than AGNCM and NLY-G.

NLY-F’s target left them a bit exposed to call risk. I wanted to pull that in a bit so that our NLY-F target would be pretty close to the price where investors would break even if shares were called immediately.

Disclosures: Long RITM-D, GPMT-A, DX-C, EFC-A, RITM-C, EFC-B, PMT-C, PMT-B, CIM-B, AGNCP, CIM-D, RITM-B, RITM, SLRC, GPMT, RC

If you enjoy this article, please tap the little heart icon. It encourages Substack to give me more visibility.

Notes About Targets

Remember that these targets already include dividend accrual.

When shares go ex-dividend, the target drops by an amount very similar to the dividend.

Further, there are some shares that are getting pretty close to expected ex-dividend dates where we still have the dividend marked as “projected”. With those shares, it’s good to double check on ex-dividend dates before trading.

Most of the shares that don’t have an announcement yet are expected to go ex-dividend around 12/28/2023.

I’ll need to see what is happening with the AAIC preferred shares as they become EFC preferred shares. Sometimes there are strange changes to the ex-dividend date in these scenarios.

New Targets and Foreshadowing

The updated targets are included below.