Industrial REIT Target Updates & Sector Update

Industrial REIT Target Updates & Sector Update

We are past due for an update an industrial REITs. Most of the discussion is available on the free side, but the parts about valuation and the individual REIT impact is reserved for paid members.

If you enjoy this article, please tap the heart icon. It doesn’t share the article. It just tells Substack that readers like our content. That lets more readers find us. If readers find us organically, I can save time on marketing and use it to produce more articles.

This article is in 4 parts:

Brief Version (public)

Long Version (public)

Target Adjustments (membership req)

Notes About Individual REITs (membership req)

We cover 4 industrial REITs presently:

Prologis: PLD (PLD)

Rexford Industrial (REXR)

Terreno Realty (TRNO)

EastGroup Properties (EGP)

The two we might add in the future are:

First Industrial (FR)

STAG Industrial (STAG)

We have no interest in covering:

Industrial Logistics Properties Trust (ILPT)

LXP Industrial Trust (LXP)

Brief Version

Industrial REITs performed better than most REITs in 2023. Market rent growth stalled, but high leasing spreads remain because current contracts are below market rate. Long-term, market rent growth should resume. AFFO per share uses current contract rates (the amount actually paid on leases), not market rates. Even if market rents were flat, there would be several years of growth in AFFO per share.

California was often the best market for industrial real estate. Not lately. It may recover if we see office conversions to multi-family. That’s still a question mark and would probably be a long process. Management in the sector is good. That’s good for long-term growth because it encourages prices above NAV. Those premiums over NAV enable accretive growth.

Overall, industrial real estate continues to perform much as expected. Treasury yields are down substantially from October, but still up relative to our prior adjustments. However, the overall environment is a bit more favorable today. All adjustments are in the range of “-5% to +4%”.

Long Version

Perhaps industrial REIT investors are simply great investors. The industrial REITs sold off in 2023 (until late October). They got pretty cheap a few times. They never got extremely cheap. The fact that industrial REITs never reached the extremely cheap level may reflect that investors have learned to have more faith in them. The investors in industrial REITs are generally focused on the long-term growth prospects. While higher interest rates are bad for AFFO per share, they are capable of reducing new projects. The combination of weak supply and intense demand should continue to drive rents higher. Of course, that doesn't mean that rents will increase every month or even every quarter. There may be some quarters where market rents do not increase. Sometimes, the market rent could even drop for a short period. However, the leasing spreads should remain dramatically positive. Many of the expiring leases are quite old. The huge leasing spreads reflect the difference between current market rates and the expiring rates. Even if market rent were flat, we would still have a substantial amount of embedded growth in net operating income and AFFO. The main reason for increased demand is the shift towards e-commerce.

E-Commerce and Industrial Real Estate

E-commerce requires dramatically more space than retail. The huge difference comes from retail sales using the retail outlet as storage. E-commerce doesn’t have the retail storage, so products usually remain in the industrial space. That’s important because each dollar of sales that moves to E-commerce drives demand (and thus rent) for industrial real estate. E-commerce is crushing physical retail stores.

Our thesis for industrial real estate is built primarily on the projected growth in market rents over the next decade. That is combined with the substantial leasing spreads to bring existing properties up to market rent. Investors who join us in industrial real estate will probably be focused on the long-term picture as well.

We are not trying to predict which month or quarter the industrial prices will increase. We are focusing on their ability to deliver dramatic growth in cash flow over time. Industrial REITs were seen as significantly exposed to recession in prior periods. That should not be the case today. They are still exposed to recessions. However, the dramatic leasing spreads should ensure the AFFO per share is always increasing (for the foreseeable future, not for eternity). Any negative growth rate for AFFO per share should be driven by non-recurring factors.

The California Factor

If we look back just a few months, the market was quite concerned about California. Because of the concern about California, we saw REITs focused on California struggling with a lower share price. Rexford Industrial is the primary example. However, over the last two months, we saw Rexford Industrial and Prologis surge higher.

I believe the case for industrial real estate in California is going to be quite interesting over the next 15 years. Industrial real estate is difficult to build in most states (especially those with more humans).

It faces severe restrictions from zoning. Further, the lower rent often makes it a less valuable use for the underlying land. We've seen a net migration out of California over the last two years. However, the actual net migration has been fairly small. Believe it or not, many people still live in California. If apartment rents became more affordable, we could see an increase in the population there.

Office Conversion and Population Density

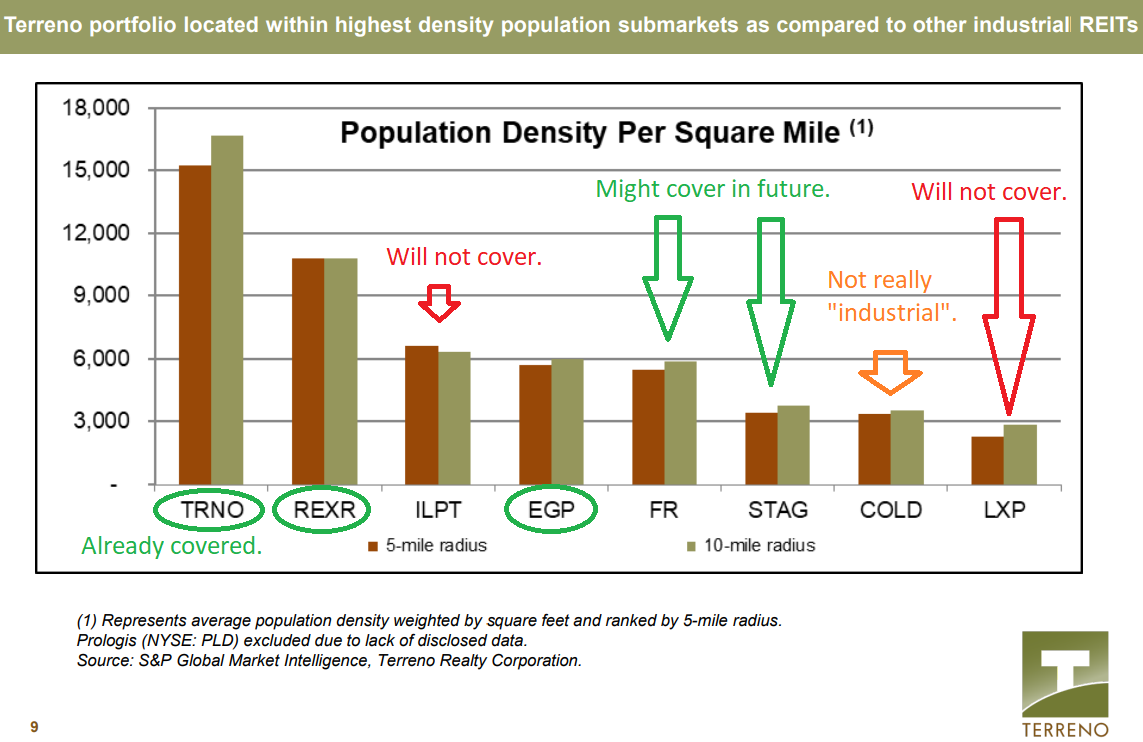

It would be possible for rents to become more affordable if there was a significant conversion from office real estate to mixed-use and residential. There is plenty of office space to be converted. However, this conversion process is only viable if the government decides that allowing housing is better than letting buildings deteriorate as they trend toward obsolescence. The government may have a hard time embracing this change. Office property often paid high levels of property taxes. Residential development often paid outrageous fees. These factors may discourage governments from permitting more conversions to residential. Office space is relevant for industrial REITs because they benefit from higher population density. Some of the industrial REITs, like Rexford and Terreno Industrial, are focused on areas where population density is extremely high.

Driving Rent Growth

The population density is a critical factor driving rent growth. Higher population density means more potential customers and less land available for industrial real estate. You cannot replace a downtown office building with an industrial location. The road structure would not match the needs of industrial property. However, if office buildings are replaced by residential buildings or mixed-use developments, it would drive population density higher. That means more potential customers who are buying crap online. That is excellent for the industrial landlords.

Supply and Demand

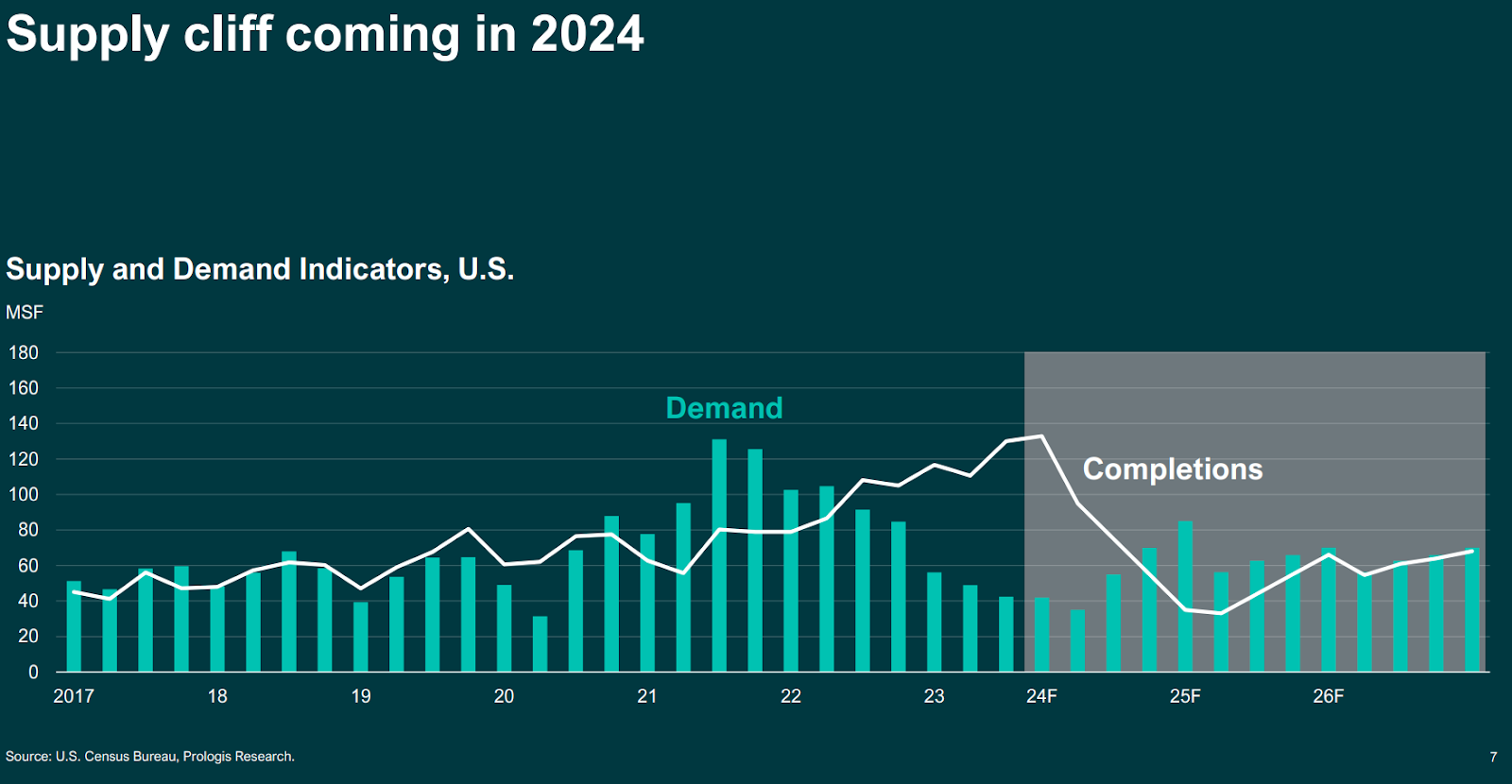

Investors may recall that I previously forecasted higher interest rates would trigger a sharp drop in industrial development. PLD is not only a huge industrial REIT; it is also a major developer. That development business drives insight into future development trends. They confirmed our expectations.

In the charts below, take a moment to verify the color of each line and what it represents. The graphics are a bit awkward because they weren’t consistent with the coloring.

For instance, in the chart below, the arrow and the words “drop in starts” should’ve been in blue to maintain the theme.

New constructions (known as “starts”) plunged as rate hikes came into play. We’re seeing the peak of completions. That means these are the most intense periods of competition for customers. This is precisely the environment where we would expect market rent growth to be most challenged.

The surge in completions was not matched with a surge in demand. However, demand should be stronger than completions in 2025, which would drive market rents higher.

Once again, this matches our expectations and reinforces our view that industrial rents should continue to grow.

PLD has been forecasting a recession all year. Consequently, they aren’t likely to give “overly optimistic” estimates for demand. I believe it is more likely that they would slightly underestimate the future demand than overestimate it.

Leadership and Growth in Industrial REITs

Industrial REITs benefit from solid leadership. That’s great for growth. Due to strong leadership (which requires a focus on shareholders), the REITs should often trade above NAV. Therefore, they should have more opportunities to issue equity and purchase new properties.

All else equal, owning 1% of $210 million of net operating income ($2.1 million) is better than owning 2% of $100 million ($2 million). That is how accretive growth works. Amateur “analysts” often misunderstand this and throw a fit about “dilution” even as the value to the shareholder improves.

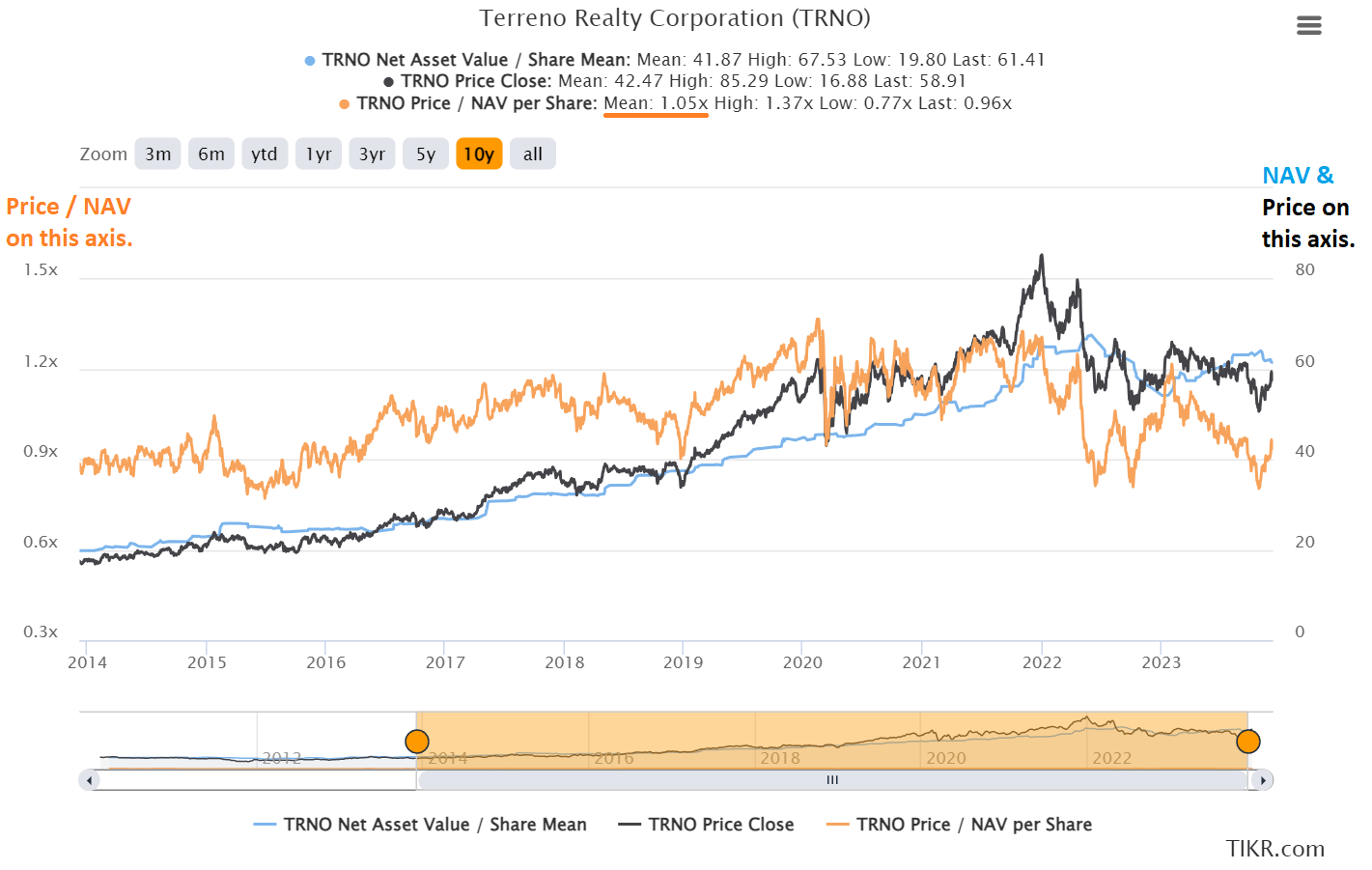

The following chart demonstrates the price to NAV for TRNO across the last 10 years:

I also pulled one that only does the last 5 years:

Debt Levels

Debt levels are low. Therefore, higher interest rates would apply to less debt. That is good.

However, higher rates can still be an important headwind because cap rates are low relative to other sectors (largely due to existing leases being below market rates). Since industrial real estate produces less net operating income today (relative to property value), there is less to cushion the impact of higher rates.

Less debt and lower cap rates generally offset each other for exposure to rates.

Rates are down compared to October, but slightly higher than during our prior dates.

Price Targets and Long-Term Expectations

The adjustment to price targets is relatively small. The industrial REITs have done what we expected them to do. They continued to deliver growth in AFFO per share while raising rents on expiring leases. Our long-term expectations remain largely similar to before. I will be interested to see how the situation in California develops. I believe many investors may be predisposed towards assuming a positive or negative outcome based on political affiliation. I would remind investors that politics is not a good investing strategy. People become emotional when they think about politics. Being emotional is a bad state of mind for someone who is logged into their brokerage account. We should be quite calm when we enter trades. A good investment is based on doing proper due diligence. Luck will play a role, but over the long term, doing proper research should outweigh luck.

Rates and Economic Position

Positive:

The economy going into 2024 looks better than it did going into 2023.

Our long-term thesis continues to function.

Interest rates are trending lower.

Negative:

Rates are still higher than they were during prior target updates.

Momentum in market rental rates stalled.

California is the most important market globally and saw more weakness.

Target Adjustments

The following table demonstrates the adjustments to targets: