Hindenburg Shorted EQIX. Was He Right?

Hindenburg Shorted EQIX. Was He Right?

If you like deep dives, you'll love this one.

Warning: This article comes in at over 3,400 words + images.

Disclaimer: We do not have a position in EQIX and do not intend to take one in the near future.

The “Conclusion” section and “Price Target Update” section (about 800 words combined) will recap the entire article. They are at the end.

So why is the article so long? Because I’m explaining and demonstrating how we reached those conclusions.

My assistant praised this article saying:

“The first few sections of the article were hard to follow. Had to read it a few times to feel like I actually understood it.”

Let’s call that praise and move on.

If you like this piece more than he did, tap the heart or the thumbs up.

Hindenburg’s short thesis on Equinix

A handful of our paid members asked us to review the short thesis on EQIX.

Sometimes reviewing a short thesis is fun because the data is organized. Other times it is dreadful because the “analyst” failed to organize or source their work.

In general, research that is poorly organized and / or poorly sourced has a huge mark against it. On the other hand, if the research is organized and sourced well, it strengthens the thesis substantially.

When research is organized and sourced, it represents more than just professionalism. It represents confidence that the thesis will withstand scrutiny. It invites anyone who disagrees to evaluate the underlying evidence themselves. If there are flaws, it would be easier to pick apart.

How does Hindenburg’s report stack up? It was well-organized and thoroughly sourced.

That also makes it more fun to dig into, because we can work much faster.

So Many Claims

The report came in at nearly 11,000 words if we include the disclaimer.

That makes my 3,400 words look concise!

Our goal is to not to evaluate every single claim, as that would become extremely slow.

We do want to dig into some of the major claims, particularly those related to metrics we can test.

This article will cover “capex” extensively. This refers to capitalized expenditures. We’ll go into greater detail throughout the article as it becomes relevant.

Boosting AFFO

That’s the core of this report.

Hindenburg says EQIX is inflating their AFFO by pretending some maintenance costs are actually enhancements.

Let’s dive into it!

I want to provide enough depth to help readers understand, without writing an entire class on the topic.

There are three big parts to emphasize, and Hindenburg only focuses on the final two.

Boosting AFFO via adjustments we would reject.

Boosting AFFO by pushing part of recurring capex through “growth” capex instead.

Problems for interconnection and power requirements.

I want to address the quicker one (point 1) first to get it out of the way.

Hindenburg took the same approach by including this portion briefly at the start, then moved on.

The First Boost: AFFO Definitions

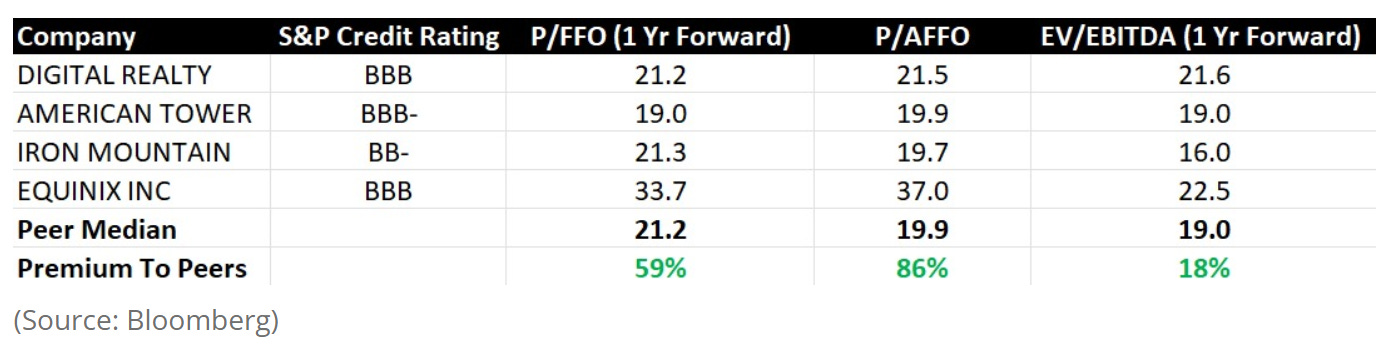

Hindenburg provides the following data, sourced from Bloomberg:

Note: This does NOT include Hindenburg’s adjustments to recurring capital expenditures!

We know this because one of the first bullet points in the report states:

“Even if you ignore the findings of our investigation and take the financials of Equinix at face value, the company trades at elevated levels; an ~86% premium to its peers on a price to forward adjusted funds from operations (“AFFO”) basis and a ~59% premium on a price to forward funds from operations (“FFO”) basis.”

Adjustments and Guidance for AFFO

To understand that chart, we really need to discuss AFFO.

I have a few metrics to provide, then I’ll walk you through them:

Management’s guidance for “AFFO” in 2024: $34.58 to $35.31 per share.

Consensus AFFO for 2024 from TIKR.com: $34.97 per share.

Implied AFFO in that table: About $22.925 per share.

From the similarity between lines 1 and 2, you can tell that the consensus AFFO estimate (from TIKR) is almost certainly matching management’s calculation method.

However, Hindenburg’s calculations are using a different method. Per Hindenburg’s commentary (quoted above), this excludes any further adjustments for recurring capital expenditures.

The Gap in AFFO

What method appears to be used?

I went through EQIX’s reconciliations and removed adjustments where I believe the adjustment results in a lower-quality calculation.

EQIX’s reported AFFO per share:

2023: $32.11

2022: $29.55

My calculations:

2023: $20.11

2022: $18.05

For comparison, FFO (not AFFO) per share:

2023: $22.66

2022: $19.89

Therefore, my values relative to FFO per share were:

2023: 88.75%

2022: 90.75%

With those data points in hand, we can evaluate the value implied from Hindenburg’s table:

2024 value implied in Hindenburg table for AFFO: $22.925

2024 consensus FFO per share: $25.17

Ratio of value implied for AFFO to consensus FFO: 91.08%

That is similar to the values I had for the last two years, so I think it’s probably a fair estimate for what I would calculate for 2024 after the numbers are all published.

The First Finding

In short, I support the premise that EQIX trades at a very high multiple of AFFO per share when adjusted to remove some of management’s calculations.

The Second Boost: Recurring Capital Expenditures

I believe this was the heart of the report.

I was swinging back and forth on this one for a bit as I dug through the evidence.

What Are Capital Expenditures?

When a company spends money to buy an asset, they “capitalize” the value onto the balance sheet.

It doesn’t go to “expenses” immediately.

There are two kinds of capital expenditures:

Recurring (or maintenance)

Growth (or expansion)

Here’s a simple example:

If you have an apartment complex and replace a roof or repave the parking lot, that is a recurring capital expenditure. It is something one must do simply to maintain the asset.

If you construct a new apartment building, then you have a growth capital expenditure. This produces new revenue.

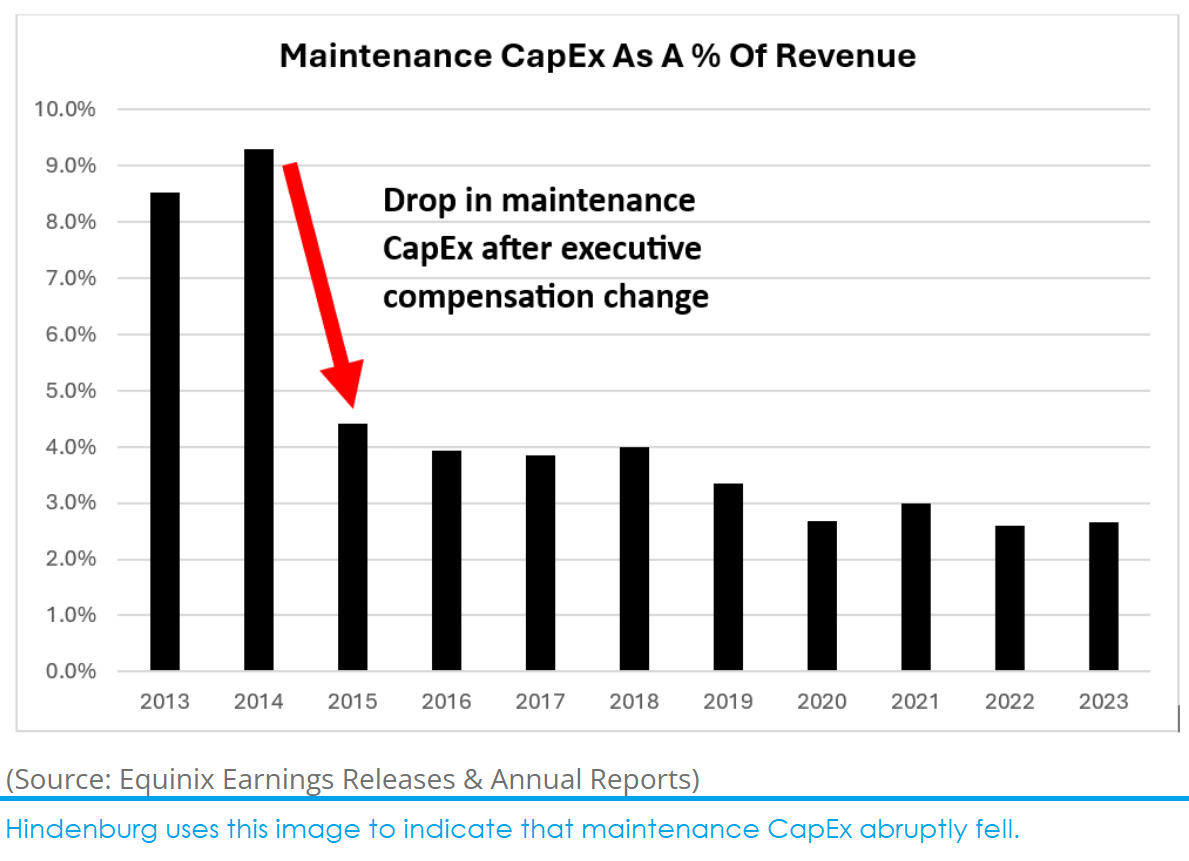

The Hindenburg Chart

This chart looks particularly bad for EQIX:

That chart looks really bad for EQIX.

However, it is reached in an interesting way.

The values for 2013 and 2014 were never actually labeled “Maintenance CapEx”.

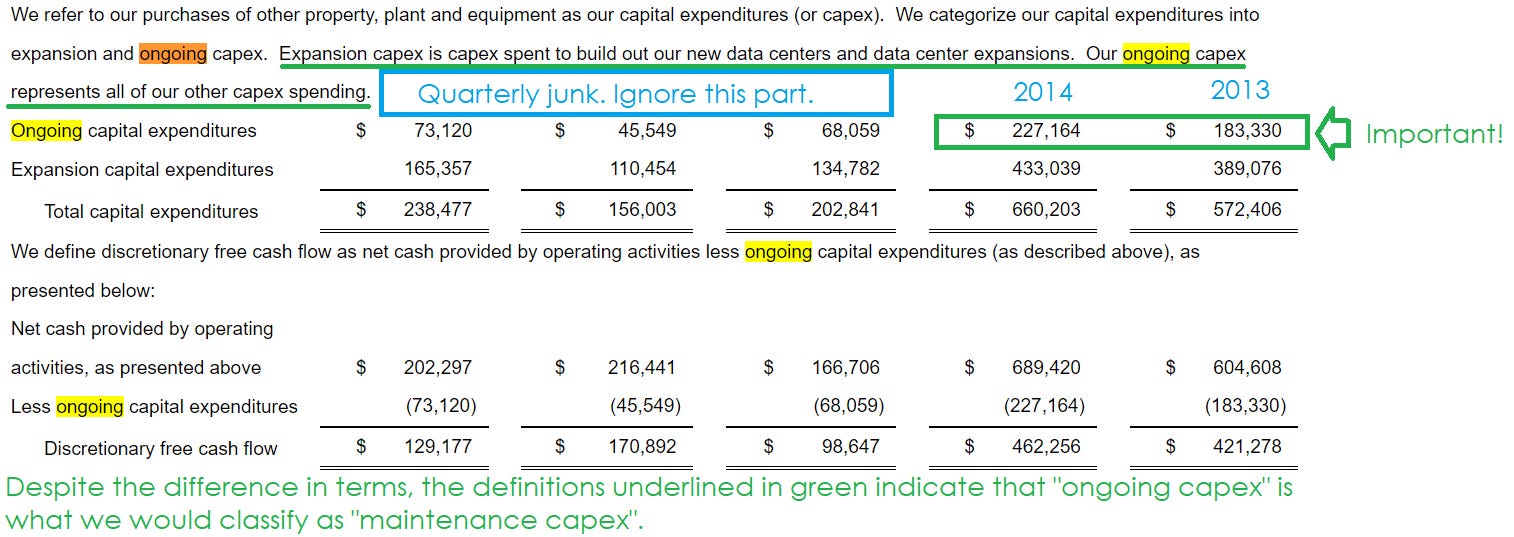

In the 2014 earnings release for EQIX, they use the term “Ongoing capital expenditures”:

After reviewing the documents, I agree with the decision to consider “ongoing capex” as equivalent to “maintenance capex”.

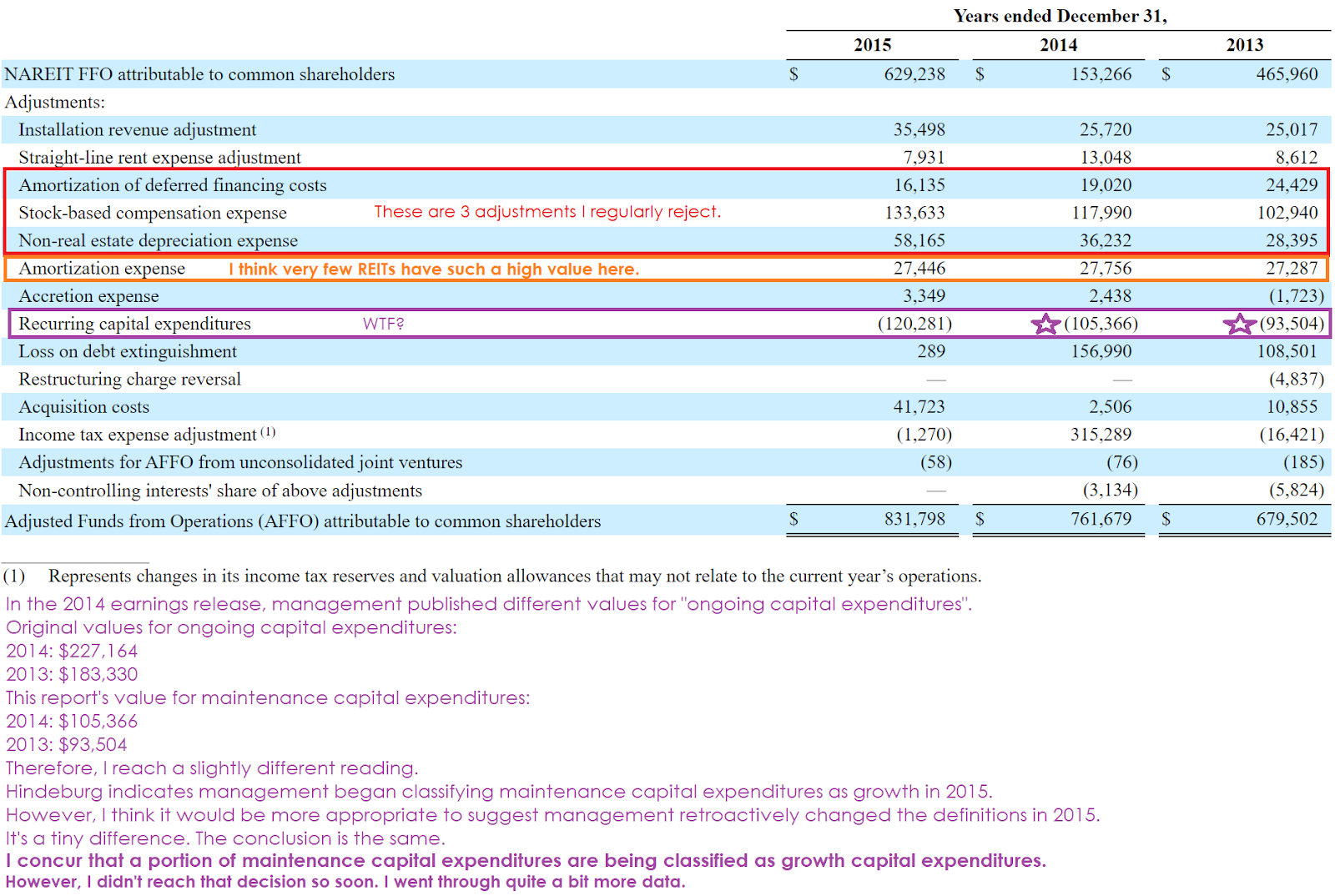

However, if we pull up the 2015 10-K for EQIX, we would find some very different values listed for those years:

Other Steps in Fact Checking

That looks pretty strange. But we wanted to be confident.