FS KKR Capital And MidCap Financial Investment’s Q4 2023 Updates By Scott Kennedy

FS KKR Capital And MidCap Financial Investment’s Q4 2023 Updates By Scott Kennedy

Introduction section by Colorado Wealth Management Fund.

Article section by Scott Kennedy.

Bringing More of Scott’s Work to Our Website

The REIT Forum is a service produced by Michael Vanloon (better known as Colorado Wealth Management Fund) and Scott Kennedy. After intense consideration, I decided to launch our service through Substack. Since then, we’ve seen great success. Substack enables us to give readers real-time alerts with entire articles delivered directly to their inboxes.

You’re probably used to seeing the “from” field saying: “ColoradoWealthManagementFund from The REIT Forum”.

In some of our future e-mails, it may say:

“Scott Kennedy from The REIT Forum”.

That will simply mean we’ve updated the backend of the website for Scott Kennedy to directly post his articles.

I want to make browsing our work as simple as possible for readers. This will be another step in that direction.

For the moment, I’ll be posting Scott’s work. The following articles are a direct copy and paste from Scott. While we get the back end set up, there is a delay in getting the articles posted. Rest assured that it should be solved soon.

Finding Our Positions

I posted a subscriber-exclusive article with links to our Google Sheets. You can always access our positions there. Scott’s positions are updated each week. CWMF’s positions are usually updated on the same day as the trade.

Disclosures

Related to the stocks in this article:

CWMF is long: RITM-D, GPMT-A, DX-C, EFC-A, RITM-C, EFC-B, PMT-C, AGNCP, CIM-D, RITM-B, RITM, SLRC, GPMT, RC.

Scott Kennedy is long: RITM, RC, SLRC, GBDC, MITT, GPMT, ARCC, RITM-D, MITT-B, MITT-C, GAINL, MFAN, ECCC.

The rest of this post is from Scott Kennedy.

This 22nd earnings assessment article reviews FSK’s and MFIC’s NAV and adjusted NII/NII performance during Q4 2023.

FSK’s NAV and adjusted NII were a minor-modest underperformance. FSK's non-accrual percentages basically doubled during the quarter (including some new non-legacy non-accrual portfolio companies).

FSK received a 2% recommendation range “downgrade”. This resulted in a risk/performance rating downgrade to 4.5. FSK is currently deemed appropriately valued (HOLD).

MFIC’s NAV matched my/our expectations while NII was a modest outperformance. No change in MFIC’s percentage recommendation ranges or risk/performance rating.

While MFIC reported a pretty good quarter, this BDC utilizes very high leverage and is deemed unattractively valued. As such, MFIC is currently deemed overvalued (SELL).

Introduction:

Hi subscribers. For new members, my name is Scott Kennedy and currently I fully cover 20 mortgage real estate investment trust (mREIT) and 15 business development company (“BDC”) common stocks within this Investing Group regarding research/data, subscriber questions, weekly projected book values/net asset values (BV/NAV), and common stock recommendation ranges. Colorado (“CO”) Wealth Management handles the mREIT preferred stocks and he and his team handles all other applicable REIT sectors outside the mREIT sector. CO also provides some mREIT common stock and BDC articles from time-to-time which are more of an “overview/introduction” discussion; typically based either on my or our combined research/data. This also includes some macroeconomic trends and data. My name is always attached to all Investing Group articles I personally wrote so there is no confusion for subscribers.

This REIT Forum article is part of a series of articles over a span of 6-7 weeks which will analyze my previously projected BV/NAV and core earnings (or core earnings equivalent)/net investment income (“NII”) figures and compare these metrics to each mREIT’s and BDC’s actual reported results, respectively. For readers who are familiar with my public mREIT and/or BDC articles, these types of articles are beneficial to readers who desire to pursue a more active investing strategy and/or want more “real time” thoughts/analysis.

I hope my services/contributions ultimately help enhance a subscriber’s total investment returns or minimize their total investment losses within the mREIT and BDC sectors. At the very least, I hope subscribers will gain more insight into the mREIT and BDC sectors by reading my/our exclusive REIT Forum articles.

1) FSK’s NAV and Adjusted NII Q4 2023 Performance (Projected Versus Actual Results):

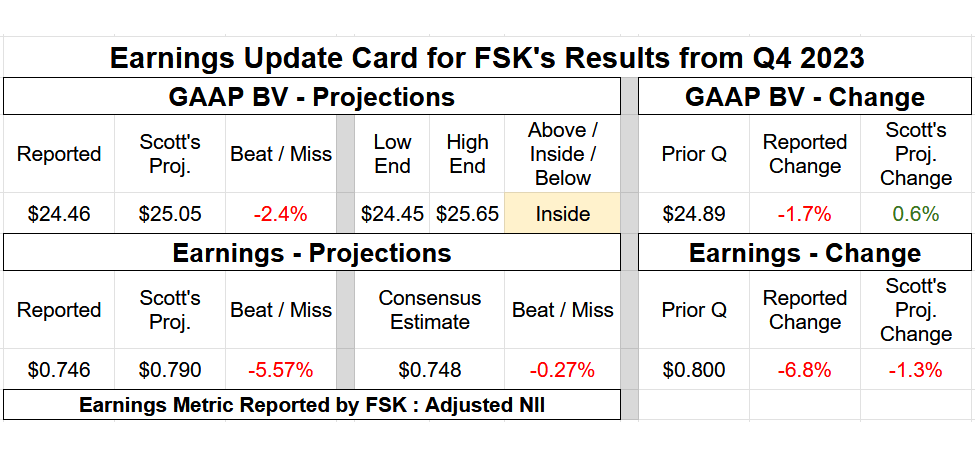

On 2/26/2024, FS KKR Capital Corp. FSK 0.00%↑ reported the company’s earnings results for the fourth quarter of 2023. Table 1 below provides FSK’s NAV and earnings summary.

Table 1 – FSK Q4 2023 NAV and Earnings Summary

Source: Taken Directly from the REIT Forum’s © Analytical Spreadsheets/Data

I provided the following commentary in regards to FSK’s results for the fourth quarter of 2023:

“Hi subscribers. I was able to review FSK’s Q4 2023 earnings results in more depth. FSK's Q4 2023 adjusted NII of $0.746 per share (NII of $0.714 per share) was a minor - modest underperformance versus my projection of $0.790 per share (range $0.745 - $0.835 per share). FSK’s Q3 2023 adjusted NII was $0.800 per share. As such, I projected an adjusted NII decrease of ($0.010) per share. In actuality, FSK reported an adjusted NII decrease of ($0.054) per share. The institutional analysts’ consensus average was adjusted NII of $0.748 per share. My preference is to use adjusted NII as this indicates FSK’s “truer” operational performance during the quarter (backs out discount accretion from the prior affiliated merger and adds back excise tax; better indication of net investment company taxable income [ICTI]).

First, let us discuss the change in FSK’s investment portfolio size. Including fair market value (“FMV”) fluctuations, FSK reduced the company’s investment portfolio size by less than ($0.1) billion during the fourth quarter of 2023. Prior to FMV fluctuations, this was through loan originations funded at close and add-on investments of $0.7 billion while recording loan prepayments/repayments/sales to its joint venture (“JV”)/restructurings of ($0.7) billion. When calculated, this was a net increase of less than $0.1 billion. In comparison, I projected a pre-FMV investment portfolio increase of $0.1 – $0.3 billion during the fourth quarter of 2023 (mean increase of $0.2 billion). So, a slightly smaller investment portfolio size when compared to my expectations.

Second, FSK maintained the company’s weighted average annualized yield during the fourth quarter of 2023 when compared to the prior quarter. However, I would point out this excludes impacts of new non-accrual loans. FSK reported a weighted average annualized yield of 12.70% for the second, third, and fourth quarters of 2023. When calculated, this was a quarterly change of 0.0%. This matched my expectations during the fourth quarter of 2023. As stated last quarter, this metric will began to plateau towards the end of 2023. In addition, it should be noted the higher LIBOR/SOFR/PRIME rose (over 500 basis points [bps] in 1.5 years), the more underlying credit risk (non-accruals) needs to be respected (and monitored). This will have heightened importance as we head through 2024.

When quantifying a smaller investment portfolio size, similar weighted average annualized yield (when excluding impacts of non-accrual loans/investments), and the impact of even more non-accrual loans/investments when compared to my expectations (discussed later), FSK reported total investment income of $447 million during the fourth quarter of 2023. When calculated, this was a quarterly decrease of ($18) million. In comparison, I projected FSK would report total investment income of $460 million. When calculated, including the incentive fee offset from lower total pre-incentive fee income, this ($13) million variance ultimately resulted in an adjusted NII underperformance of ($0.041) per share when compared to my expectations.

When this variance is combined with a remaining ($0.003) per share adjusted NII underperformance within FSK’s expense accounts (deemed immaterial to discuss this quarter [remember non-accrual loans/investments have no offsetting impact regarding interest expense]), this fully reconciles to FSK’s adjusted NII underperformance of ($0.044) per share during the fourth quarter of 2023 when compared to my expectations.

Moving on, FSK reported a NAV as of 12/31/2023 of $24.46 per share (1.7% decrease) versus my projection of $25.05 per share (0.6% increase). I consider this a minor (at or greater than a 1.0% but less than a 2.5%) – modest underperformance and was within my $24.45 - $25.65 per share range (at the low end). As such, unlike the prior quarter, I was a bit disappointed with FSK’s NAV performance this quarter (an underperformance versus the broader BDC sector average).

When taking a “run through” of FSK’s investment portfolio, there were a handful of valuation surprises. Since FSK had 204 portfolio companies as of 12/31/2023, it will take some time to fully review the entire investment portfolio. That said, I did review FSK’s non-accrual loans and some more material investments. Regarding credit metrics, FSK put 5 new portfolio companies on non-accrual status during the fourth quarter of 2023. These portfolio companies were Kellermeyer Bergensons Services LLC (Kellermeyer), Miami Beach Medical Group LLC (Miami Medical), Reliant Rehab Hospital Cincinnati LLC (Reliant), Sweeping Corp of America Inc. (Sweeping), and JW Aluminum Co (JW Aluminum). I correctly anticipated Kellermeyer, Reliant, and JW Aluminum (which is actually a preferred stock position; stopped accruing dividends) would be placed on non-accrual status during the quarter. Regarding Miami Medical, while I already knew this portfolio company was experiencing some credit risk, I did not anticipate this portfolio being placed on non-accrual status during the fourth quarter of 2023. I assumed this event would occur during 2024. Regarding Sweeping, this portfolio company being placed on non-accrual status was a surprise. When combined, the total amortized cost balance of FSK’s new non-accrual loans/investments was $654 million during the fourth quarter of 2023. Simply put, a notable increase was is a negative catalyst/trend. In comparison, I projected new non-accrual loans/investments of $455 million. On a bit of brighter news, to remain non-bias I was pleased FSK’s second first lien debt investment with Tangoe LLC (Tangoe), with a principal balance of $179.5 million as of 12/31/2023, was not put on non-accrual status during the quarter. This was a portfolio company I have discussed the past couple of quarters. That said, this specific loan is still exhibiting some credit risk and could possibly be placed on non-accrual status down-the-road. As such, heightened monitoring will need to continue to occur.

In addition, 2 portfolio companies were taken off non-accrual status, Matchesfashion Ltd (Matchesfasion) and Sungard Availability Services Capital Inc. (Sungard). Both portfolio companies were sold/written-off during the quarter for a very small net realized loss (deemed immaterial to discuss further). As a reminder, FSK mostly/fully wrote-off the company’s investments in Monitronics International Inc. (Monitronics), ThermaSys Corp. (ThermaSys), and Hilding Anders (Hilding) during the second quarter of 2023 which resulted in notable net realized losses.

As of 9/30/2023, FSK’s non-accrual percentage, based on amortized cost basis and FMV, was 4.8% and 2.4%, respectively. As of 12/31/2023, FSK’s non-accrual percentage, based on amortized cost basis and FMV, increased to 8.9% and 5.5%, respectively. Regarding a BDC stock, this should be considered a modest – notable quarterly increase in non-accruals (a negative factor/trend).

Getting back to the numbers, within FSK’s entire investment portfolio, the company recorded a net realized gain and unrealized depreciation of ($110) million during the fourth quarter of 2023. In comparison, I projected FSK would report a net realized loss and unrealized appreciation of $40 million. When calculated, this ($151) million variance (rounded) directly led to a NAV underperformance of ($0.55) per share when compared to my expectations.

When the variance noted above is combined with no NAV fluctuation directly due to no stock being repurchased during the fourth quarter of 2023 (no equity accretion) and the adjusted NII underperformance of ($0.044) per share discussed earlier, this directly reconciles to FSK’s NAV underperformance of ($0.59) per share when compared to my expectations.

So, all-in-all, a minor - modest underperformance on FSK’s adjusted NII (variance of $0.044 per share) and the company’s NAV (variance of 2.3%). Regarding dividends, FSK declared an unchanged “base” dividend of $0.64 per share for the first quarter of 2024 while also declaring an unchanged special periodic dividend of $0.06 per share. In addition to these 2 declarations, FSK previously declared an “extra special” periodic dividend of $0.05 per share over 2 quarters during 2024. When combined, an unchanged total quarterly dividend of $0.75 per share when compared to the prior quarter. Simply put, these declarations were not a surprise and were within my/our previously projected range. FSK has continued to have a modest – fairly large cumulative undistributed taxable income (“UTI”) balance. This even factors in the more recent special/extra special periodic dividends which technically “take a bit more out” of FSK’s quarterly cumulative UTI balance. This simply means FSK’s taxable income has “kept pace” with the recent total amount of quarterly dividend distributions. In my opinion, this was the best news this quarterly cycle for FSK.

So, I believe FSK reported a bit of a disappointing quarter on both NII/adjusted NII and NAV. One also has to consider the company now has 15 portfolio companies with at least 1 debt investment on non-accrual status as of 12/31/2023. I would like to see some partial, near-term recoveries on these particular non-accrual loans (not just write-offs similar to what occurred during the second quarter of 2023). In addition, FSK’s “payment-in-kind” (“PIK”)/deferred income remained high at 8% of the company’s total investment income during the fourth quarter of 2023. That said, to remain non-bias, this was a modest decrease from 12% during the third quarter of 2023. However, this PIK/deferred income decrease was directly associated with the aforementioned handful of new non-accrual portfolio companies (previous PIK/deferred income now placed on non-accrual status) which is not the best outcome for a reduction in this metric.

When looking back to my thoughts last quarter, in relation to not upgrading FSK after reporting an encouraging third quarter of 2023, I am glad I remained cautious with this BDC as the company reported a bit of a disappointing fourth quarter of 2023. Remember, FSK already has the 2nd largest percentage recommendation range discounts in the BDC sector. Simply put, I/we continue to believe FSK will underperform the company’s BDC sector peers over the long-term. Therefore, when taking FSK’s recent and projected performance into consideration, along with macroeconomic trends/events (mainly Fed monetary policy, the general projected movement of rates/yields, and projected economic performance over the foreseeable future), I/we are “downgrading” our FSK percentage recommendation ranges (relative to CURRENT BV) by (2%). This change is already reflected in the subscriber spreadsheets (resulted in a price target decrease of approximately ($0.50) per share). This also results in a downgrade to FSK’s risk/performance rating from 4 to 4.5.

At a closing price as of 2/28/2024 of $18.54 per share, FSK is deemed to be APPROPRIATELY VALUED/a HOLD recommendation (price target of $20.70 per share). Therefore, FSK is not one of the most overvalued BDCs in my/our opinion but currently is not one of the most undervalued either. Looking back, I am glad I exited my FSK position on 12/11/2023 at a weighted average sales price of $20.49 per share. This trade was disclosed to subscribers in “real time” (the day of my trade)…”

2) MFIC’s NAV and NII Q4 2023 Performance (Projected Versus Actual Results):

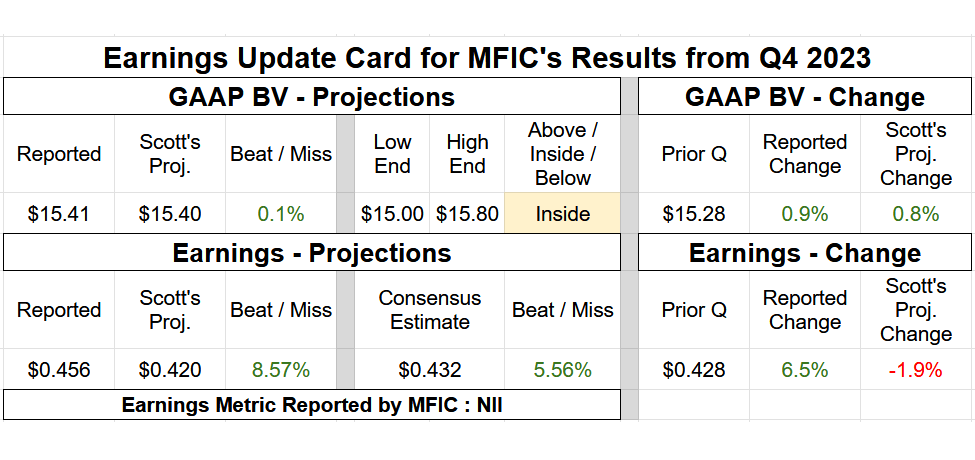

On 2/26/2024, MidCap Financial Investment Corp. MFIC 0.00%↑ reported the company’s earnings results for the fourth quarter of 2023. Table 2 below provides MFIC’s NAV and earnings summary.

Table 2 – MFIC Q4 2023 NAV and Earnings Summary

Source: Taken Directly from the REIT Forum’s © Analytical Spreadsheets/Data

I provided the following commentary in regards to MFIC’s results for the fourth quarter of 2023:

“Hi subscribers. I was able to review MFIC’s Q4 2023 earnings results in more depth. MFIC’s Q4 2023 net investment income (“NII”) of $0.456 per share was a modest outperformance versus my projection of $0.420 per share (range $0.395 - $0.445 per share). MFIC’s NII was $0.428 per share for the third quarter of 2023. As such, I projected a NII decrease of ($0.008) per share. In actuality, MFIC reported a NII increase of $0.028 per share during the fourth quarter of 2023. The institutional analysts’ consensus average was NII of $0.432 per share. Let us reconcile MFIC’s modest quarterly NII outperformance.

First, let us review MFIC’s quarterly investment activity. MFIC recorded loan originations funded at close and add-on investments of $16 and $114 million during the third and fourth quarter of 2023, respectively. As such, as correctly anticipated, a nice quarterly “uptick” in origination/funding volume. In comparison, I projected quarterly loan originations funded at close and add-on investments of $75 - $125 million (mean of $100 million). MFIC recorded loan prepayments/repayments/restructurings of ($59) and ($152) million during the third and fourth quarter of 2023, respectively. In comparison, I projected quarterly prepayments/repayments/restructurings of ($125) – ($175) million (mean of ($150) million). When calculated, excluding fair market value (“FMV”) fluctuations, MFIC decreased the company’s investment portfolio size by ($39) million (rounded) during the fourth quarter of 2023. In comparison, I projected MFIC would decrease the company’s investment portfolio size by a mean of ($50) million. This directly led to a slightly higher amount of quarterly accrued interest income due to a very slightly larger investment portfolio size. When calculated, including the incentive fee offset from higher total pre-incentive fee income, this ultimately resulted in a NII outperformance of $0.004 per share when compared to my expectations.

Second, unlike some sector peers, MFIC continued to experience a rise in the company’s weighted average annualized yield during the fourth quarter of 2023 when compared to the prior quarter. Simply put, this was even with the recent “plateauing/leveling off” in LIBOR/SOFR/PRIME. This was a bit of a positive surprise. MFIC reported a weighted average annualized yield of 11.80%, 12.00%, and 12.10% for the second, third, and fourth quarter of 2023, respectively. When calculated, this was a quarterly increase of 0.2% and 0.1%, respectively. This past quarter, this was a 0.2% outperformance when compared to my expectations. That said, as stated last quarter, this metric will began to plateau towards the end of 2023. In addition, it should be noted the higher LIBOR/SOFR/PRIME rose (over 500 basis points [bps] in 1.5 years), the more underlying credit risk (non-accruals) needs to be respected (and monitored). This will have heightened importance as we head through 2024. When quantified, including the incentive fee offset from higher total pre-incentive fee income, this directly led to a NII outperformance of $0.038 per share when compared to my expectations.

When the 2 variances noted above are combined, along with a NII underperformance of ($0.006) per share within all non-incentive fee expense and fee waiver accounts (mainly slightly higher-than anticipated base management fees and interest expense from a slightly larger investment portfolio size), this fully reconciles to MFIC’s NII outperformance of $0.036 per share during the fourth quarter of 2023 when compared to my expectations.

On a side note, MFIC’s leverage of 1.45x as of 12/31/2023 remains well above the 15 BDC peer average I/we cover which remains a bit troubling. MFIC’s leverage ratio as of 12/31/2023 was likely the 2nd highest out of all covered BDC peers (awaiting TPVG’s results who likely continued to have the highest). MFIC’s leverage needs continued monitoring. As a reminder, a BDC’s regulatory leverage cap. is currently 2.00x. For comparative purposes, the 15 BDC peers I/we currently cover had an average leverage ratio of only ~1.10x as of 12/31/2023.

Moving on, MFIC reported a net asset value (“NAV”) as of 12/31/2023 of $15.41 per share (0.9% increase) versus my projection of $15.40 per share (0.8% increase). I consider this basically an exact match (at or within a 0.5% variance) and was well within my $15.00 - $15.80 per share range.

When factoring in MFIC’s $0.036 per share NII outperformance, this calculates to a ($0.03) per share NAV underperformance strictly within the valuation fluctuations of the company’s investment portfolio when compared to my expectations. This very minor NAV underperformance was simply scattered amongst MFIC’s 152 portfolio companies as of 12/31/2023. Upon a quick review, there were no notable surprises in any 1 portfolio company when compared to my expectations. Regarding MFIC’s entire investment portfolio, the company recorded a combined net realized gain and unrealized appreciation of $3 million during the third quarter of 2023. In comparison, I projected a combined net realized gain and unrealized appreciation of $5 million. When calculated, this ($2) million variance directly led to a NAV underperformance of only ($0.03) per share when compared to my expectations.

When the variance noted above is combined with MFIC’s NII outperformance of $0.036 per share discussed earlier and a matching of equity balance sheet activity (no shares issued or repurchased), this fully reconciles to the company’s NAV outperformance of $0.01 per share during the fourth quarter of 2023 when compared to my expectations.

Regarding credit risk, as correctly anticipated, MFIC put 0 new portfolio companies on non-accrual status during the fourth quarter of 2023 (as highlighted in our weekly mREIT and BDC article series/newsletter). In addition, 0 portfolio companies were taken off non-accrual status during the quarter. I continue to believe there will be a general rise in credit risk during 2024 so this is just something to take note of.

So, all-in-all, a modest outperformance on MFIC’s NII (variance of $0.036 per share) and basically an exact match on the company’s NAV (variance of only 0.1%). I would say a pretty good quarter for MFIC (nice bounce back on the NII side of the equation). I was also pleased MFIC’s capitalized payment-in-kind (“PIK”)/deferred income percentage remained very low – low (below the BDC sector average). In addition, Merx Aviation Finance LLC (“Merx”) has continued to stabilize operational performance which is “cautiously optimistic” at this point in time. Merx is in the process of slowly deconsolidating/shrinking the company’s operations.

As noted 6 quarters ago, MFIC announced a change in general strategy to basically solely focus on lending to “safer” portfolio companies. This included a new partnership/equity sponsor with MidCap Financial, an affiliate of MFIC’s external manager, Apollo Global Management, Inc. In addition, this fairly recently included a notable base management fee reduction (based on equity versus assets) which started on 1/1/2023. This directly resulted in my/our modest percentage recommendation range (relative to CURRENT NAV) upgrade back in late 2022.

As noted last quarter, MFIC has entered into merger agreements with 2 affiliates, Apollo Senior Floating Ratio Fund Inc. AFT 0.00%↑ and Apollo Tactical Fund Inc. AIF 0.00%↑ . I previously performed a fairly detailed internal AFT and AIF review. AFT and AIF also mainly invest in private, middle market (“MM”) loans. Both entities also have some broadly syndicated loans, structured credit, and equity investments. As such, the merging of these affiliate companies should not be overly complicated/move MFIC away from the company’s niche investments. These mergers will probably result in a very slight benefit to MFIC through operational synergies and a slight reduction in operational costs of the combined investment portfolios. However, not beneficial enough yet to warrant an upgrade in my professional opinion. AFT and AIF are currently generating yields below MFIC by a pretty good margin. Also, as noted above, I/we already modestly upgraded MFIC on the company’s base management fee reduction and shift to less risky loans back in late 2022. AFT and AIF both have non-accrual percentages higher than MFIC.

When taking MFIC’s recent and projected performance into consideration, along with macroeconomic trends/events (mainly Fed monetary policy, the general projected movement of rates/yields, and projected economic performance over the foreseeable future), no change to my/our MFIC percentage recommendation ranges (relative to CURRENT NAV) or risk/performance rating (remains at a 4). Countering low capitalized PIK/deferred income and stable performance from Merx, I remain a bit concerned on MFIC’s very high leverage and the risk of additional non-accrual portfolio companies during 2024. Due to MFIC’s high leverage, this BDC continues to have modestly – notably less “leeway” regarding increasing leverage in the future (especially if the company continues to trade at a discount to CURRENT NAV). This will likely “crimp” quarterly NII whereas other BDC peers can take up leverage as rates/yields eventually decrease looking further out on the time horizon. We will see how much the AFT and AIF merger helps regarding reducing leverage at some point during 2024 (still requires shareholder approval; date not yet set). If MFIC reports an outperforming first quarter of 2024 while reducing leverage some, this BDC would likely receive an upgrade next quarter (just a “heads up”).

At a closing price as of 2/28/2024 of $14.59 per share, MFIC is deemed to be modestly OVERVALUED/a SELL recommendation (price target of $13.40 per share). Currently, MFIC is not the most overvalued BDC stock that I/we cover but, in my opinion, is far from being the most undervalued either. Currently, until MFIC presents a more attractive valuation, I would look elsewhere regarding a potential BDC investment…”