Alexandria Q2 2025 Update

Alexandria Real Estate (ARE) reported Q2 2025 results after the market closed 7/21/2025.

Our Position

We have a small position in ARE. Shares look cheap, but headwinds will likely persist for years. Consequently, we've been building our position very gradually.

Wall Street’s Definitions for FFO (Repeated for ARE)

Words are bad. They are imprecise. I used to explain the differences in words. I hated it.

I built a chart to explain the concept.

We will primarily be discussing FFO As Adjusted (Value 2) in this article. However, when we look at valuation, we place a greater emphasis on AFFO (Value 3).

Results for FFO As Adjusted / Wall Street FFO (Value 2)

- Consensus FFO estimate: $2.29

- FFO Result: $2.33

- Nice beat on FFO As Adjusted.

- Note: Some sites incorrectly reported “FFO As Adjusted” as “AFFO”. If you see a site reporting $2.33 for “AFFO”, you’ve found a site that doesn’t understand the difference.

Guidance for FFO as Adjusted (Value 2)

- Old Guidance for 2025 FFO: $9.16 to $9.36 (midpoint $9.26)

- New Guidance for 2025 FFO: $9.16 to $9.36 (midpoint $9.26)

- Change: $0.00.

- Consensus Estimate for 2025 before release: $9.20 (down from $9.28 before Q1 2025 release).

- Guidance is $.06 above the consensus estimate.

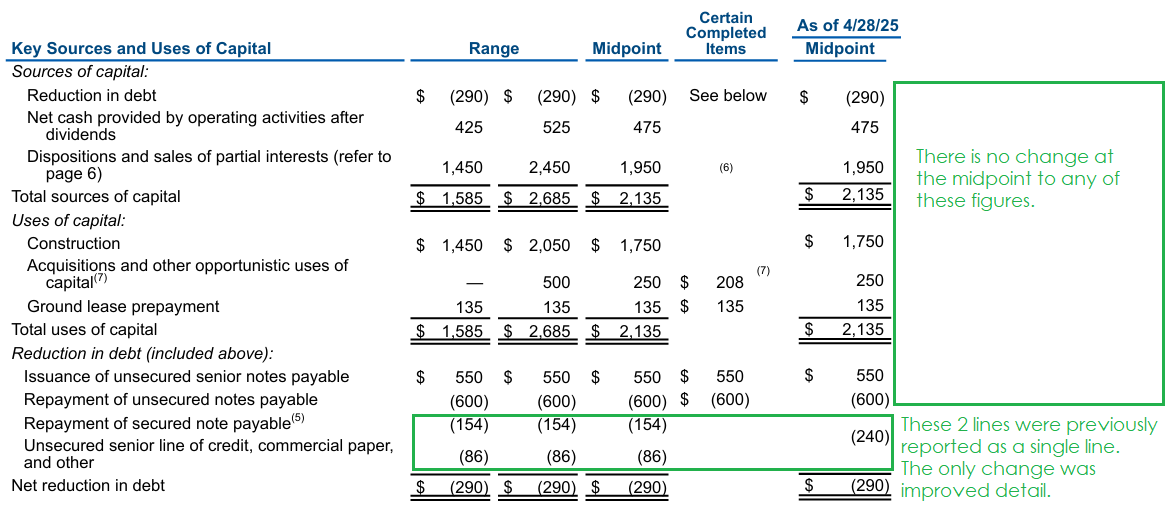

Unchanging Capital Allocation

In the Q1 2025 release, ARE announced some changes to their capital allocation plan. I liked the Q1 2025 changes.

In the Q2 2025 release, ARE maintained the same expectations they laid out in Q1 2025. Good choice. Further changes were not needed.

Source: Alexandria Real Estate, green boxes / notes by author.

The ATM Program and Buybacks

In Alexandria’s Q4 2024 release (and technically in an announcement before that) management announced a buyback program for up to $500 million.

- Q4 2024: Alexandria used $50.1 million on buybacks in December 2024 (thus $50.1 million for Q4 2024).

- Q1 2025: Alexandria used another $150 million through late January.

- Q1 2025: Alexandria used about $58 million during the rest of Q1 2025 (thus $208 million in Q1 2025).

- Q2 2025: No shares repurchased during Q2 2025.

- Q2 2025: No shares repurchased through July 21, 2025.

I think ARE missed an opportunity for buybacks. There’s a very simple strategy for buybacks when trading at a large discount to consensus NAV. It is a strategy many companies may overlook in favor of splashier moves. The strategy goes like this:

- Establish a rough goal for buybacks. It can be less than the max in the buyback program.

- Establish a target period for those buybacks. For instance, they could target $252 million in 2025.

- There should be about 252 market days in 2025. Therefore, they would aim for $1 million per day.

- Establish a price ceiling. If the price is above that ceiling, no buybacks for that day.

We don’t want management to spend their time trying to figure out the exact bottom for the share price. Their job is running the company. This is a job where dollar cost averaging can work quite well.

Leasing Spreads

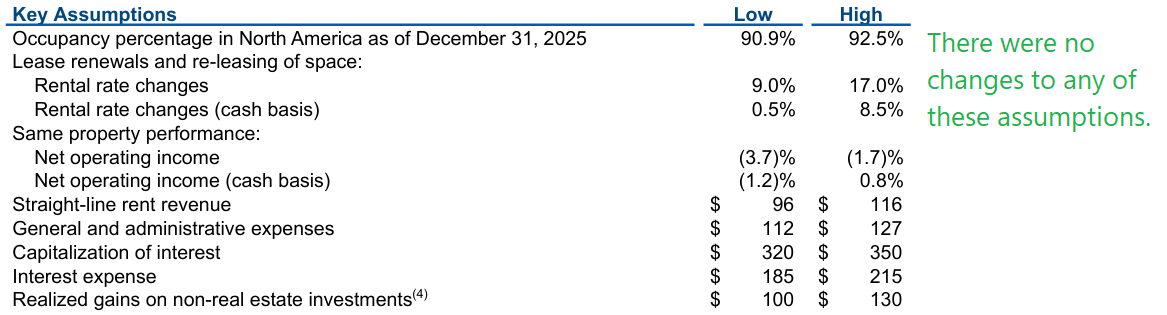

Guidance for 2025 full-year leasing spreads was unchanged:

- GAAP spreads: 9% to 17%

- Cash spreads: 0.5% to 8.5%

Spreads for leases during this quarter were:

- GAAP spreads: 5.5%

- Cash spreads: 6.1%

The cash spreads were still above the middle of the range. The GAAP spreads were low, but are offset by strong GAAP spreads in Q1 2025. Spreads for leases across the first half of the year:

- GAAP spreads: 13.2%

- Cash spreads 6.9%

Note: The leasing volume (amount of feet leased) in Q2 2025 was low. This was a factor in occupancy dipping from 91.7% (end of Q1 2025) to 90.8% (end of Q2 2025). However, July 2025 started off with a big 16-year lease, which should give Q3 2025 a better start for total leasing volume.

Other Guidance Items

Other items were unchanged.

Source: Alexandria Real Estate

Earnings Call

The earnings call is scheduled for 2:00 p.m. Eastern Time on 7/22/2025. In other words, it hasn’t started yet.

Conclusion

The beat on FFO As Adjusted was nice. Guidance being maintained was also positive. ARE is priced as a REIT facing significant, but not massive, challenges. I expect they will eventually fight their way out of this environment, but it will take years due to the excess supply of lab science brought to market by speculative developers. Tenants simply have quite a few options for where to lease. ARE has great locations, which can mitigate some of the pressure, but it still has a significant impact on occupancy and leasing spreads.

Due to the excess supply, ARE’s FFO As Adjusted per share will likely have minimal (or negative) growth over the next few years. To completely absorb the excess supply in the market will most likely take several years with less development activity. ARE would be wise to encourage local governments to restrict development of lab space under threat of appealing property tax rates due to declining real estate market values.

I believe ARE’s FFO As Adjusted per share will be flat to slightly down over the next few years. The company trades around a 6.6% dividend yield and an AFFO multiple (not FFO As Adjusted) just under 11x. That’s the valuation you see when the market is heavily concerned about the growth prospects for a REIT.

Can ARE return to growing AFFO and FFO As Adjusted? Probably. I wouldn’t expect it soon though. The stock pays out a solid dividend yield while investors wait for the leasing environment to improve. For some investors, waiting a few years for growth in AFFO or FFO as Adjusted will be too long. For others, it’s an opportunity to get a big yield with long-term upside.

Overall, this was a positive earnings release.

Disclosure: Long ARE.

Member discussion